The conflicts erupting across Turkey's neighborhood are doing more than reshaping political maps. They are quietly redrawing the region's energy geography, forcing countries to reroute pipelines, seek alternative corridors, and settle for less efficient solutions. For Turkey, these pressures simultaneously create opportunities and expose the structural limits of its longstanding ambition to become a regional energy hub.

Turkish President Recep Tayyip Erdoğan sent a written message to the 30th Baku Energy Week in which he offered a summary of his government's energy diplomacy. He pointed to the Azerbaijani gas flowing into Syria since August 2025 as an example of Turkey's stabilizing role, described the prospect of exporting Turkmen gas through Azerbaijan and Turkey as a major opportunity, and highlighted the growing use of the Baku-Tbilisi-Ceyhan (BTC) pipeline to bring Kazakh crude to Western markets. These remarks reflect a genuine shift in regional energy flows and Turkey's expanding role as an energy corridor. But each also comes with its constraints.

Turkey's energy hub ambition has always rested on a premise that the surrounding environment would be stable enough to support the long-term infrastructure investment that hub status requires. Nonetheless, regional wars are disrupting existing energy routes and may also be foreclosing the routes that do not yet exist.

Kazakhstan and the Long Way Around

Kazakhstan's experience since 2022 illustrates how conflict can alter energy routing decisions. Before Russia's full-scale invasion of Ukraine, approximately 80 percent of Kazakh oil exports passed through Russian territory, reaching the Black Sea port at Novorossiysk via the Caspian Pipeline Consortium (CPC) pipeline. That route has become increasingly problematic. Ukrainian drone and naval strikes targeting Russian energy infrastructure — what Kyiv has described as part of its "long-range sanctions" strategy — have directly affected the CPC terminal on multiple occasions. In November 2025, Ukrainian uncrewed surface vessels struck the CPC's SPM-2 mooring unit, causing serious damage and halting oil loadings entirely. In April 2026, Ukrainian drones struck energy export infrastructure around Novorossiysk again. Russia said the CPC terminal was damaged, while Ukrainian officials said six of seven tanker-loading stands at the nearby Sheskharis terminal were hit. Kazakhstan formally protested to Kyiv, calling these strikes acts of aggression against a civilian facility, but the vulnerability of the route remains.

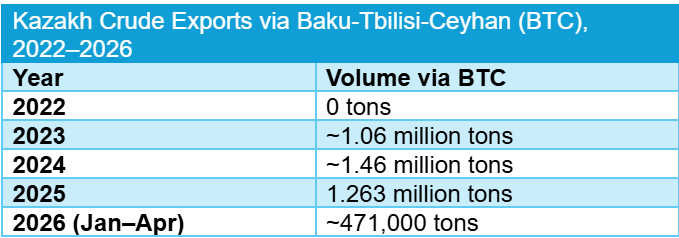

Kazakhstan's response has been to ship oil across the Caspian Sea by tanker to Azerbaijan and then westward through the BTC pipeline to Ceyhan. From zero in 2022, volumes rose to 1.06 million tons in 2023, peaked at 1.46 million tons in 2024, and settled at 1.263 million tons in 2025. Plans to raise the annual ceiling from 1.5 to 2.2 million tons are underway.

The increasing use of the BTC pipeline by Kazakhstan deepens Turkey's ties with the Central Asian Turkic states. For Ankara, it is also a demonstration of Turkey's value as a transit country. However, the route is a workaround, not an optimal solution. The Caspian tanker crossing covers only around 360 kilometers, which is economically viable for oil but barely acceptable by efficiency standards.

A pipeline would resolve the efficiency issue. Yet the problem is not a technical one but legal and political. The five Caspian littoral states signed the Convention on the Legal Status of the Caspian Sea in 2018, but seabed delimitation remains unresolved. Russia and Iran have consistently opposed a trans-Caspian pipeline, citing environmental concerns as well as the straightforward geopolitical interest in preventing a new energy corridor that bypasses their territory.

Turkmen Gas: The Structural Bottleneck

If Kazakhstan's oil story shows the possibilities of adapting existing infrastructure, Turkmenistan's gas story illustrates the harder limits of geography and geopolitics. Erdoğan's reference to the export of Turkmen gas through Azerbaijan and Turkey points to a long-held aspiration. Turkmenistan holds the world's fourth-largest natural gas reserves, yet remains almost entirely dependent on a single export route to China. Breaking this dependency and connecting Turkmen gas to European markets via Turkey would serve multiple interests simultaneously — Ankara's hub ambitions, Ashgabat's diversification goals, and Europe's desire to reduce dependence on Russian gas.

In early 2025, Turkey and Turkmenistan signed a swap deal under which Turkmenistan supplies gas to northeastern Iran, and Turkey receives an equivalent volume through the existing Iran-Turkey pipeline. The agreement, between state pipeline operators BOTAŞ and Turkmengaz, provides for up to 2 billion cubic meters (bcm) annually.

This was a genuine step forward. But it was also structurally fragile. The deal relies entirely on Iranian infrastructure, which is subject to chronic underinvestment, seasonal disruptions, and Western sanctions that could tighten further. Furthermore, 2 bcm is modest relative to Turkey's total gas consumption of roughly 60 bcm annually. Transporting larger volumes through Iran would require a level of Iranian cooperation that cannot be taken for granted. The more durable solution — a Trans-Caspian Pipeline connecting Turkmenistan directly to Azerbaijan — remains blocked due to the status of the Caspian Sea discussed above.

The 2026 Iran war, which began on February 28, has made this calculus even starker. Israel struck the South Pars gas field on March 18, 2026 — halting production at the Asaluyeh processing hub, a field supplying 70 percent of Iran's domestic gas consumption. Iran retaliated by attacking critical energy infrastructure across the Gulf, threatening to do more if war continued. Iran has also closed the Strait of Hormuz to maritime traffic. A country actively targeting energy infrastructure as a weapon of war in an ongoing conflict may not passively accept a new pipeline running beneath the Caspian without its consent.

Azerbaijani Gas and Syria's Electricity Crisis

The third element in Erdoğan's message concerns Syria. On August 2, 2025, Turkey, Azerbaijan, Qatar, and Syria formally inaugurated the Turkey-Syria Natural Gas Pipeline, connecting Kilis in southern Turkey to Aleppo in northern Syria. The gas is sourced from Azerbaijan. The project is financed by Qatar through its Qatar Fund for Development, and follows agreements reached between Azerbaijani President Aliyev and Syrian President Ahmad al-Sharaa in 2025.

The arrangement is notable in several respects. Despite Azerbaijan's close ties with Israel, Ankara persuaded Baku to participate in an initiative that serves the newly established Syrian government. The gas restarts power plants in areas long suffering from electricity shortages caused by more than a decade of civil war. Thanks to natural gas provided through Turkey and Jordan, Damascus, Aleppo, and Hama were receiving between 16 and 24 hours of electricity per day — up from the 4–6 hours that had been the norm for years. This is a tangible early achievement of the new Syrian administration. Nonetheless, Syria's electricity infrastructure still requires large investment to meet increasing demand.

Iraqi Oil and New Pipeline Plans

Regional disruption has also prompted new projects. With the Strait of Hormuz effectively closed, Iraq's oil production has collapsed from around 4.3 million barrels per day (bpd) to roughly 1.4 million bpd. With petroleum revenues accounting for 90 percent of the state budget, Baghdad looks for alternatives. On March 17, 2026, Iraq's federal government and the Kurdistan Regional Government reached a deal to resume crude exports through the Kirkuk-Ceyhan pipeline, with initial flows of 200,000–250,000 bpd commencing the following day. In early June 2026, the Iraqi government approved a plan to nearly triple its crude exports through the Kirkuk-Ceyhan pipeline, targeting up to 770,000 bpd within two and a half months — up from the initial 250,000 bpd resumed in March. The Iraqi government is also considering an extension of this Kirkuk-Ceyhan pipeline southward to Basra.

Turkey operates in an energy ecosystem built around existing infrastructure under suboptimal conditions, in a region where optimal conditions may not return soon. Ankara benefits from the rerouting pressures created by war, sanctions, and infrastructure insecurity. Yet these gains rely largely on existing pipelines, limited volumes, politically fragile arrangements, and second-best routes. Turkey’s energy relevance is therefore rising, even if the structural conditions required for genuine hub status remain absent.