An energy hub confers logistical advantages as well as geopolitical power, a reality demonstrated by Europe’s commitment to reduce its overdependence on Russian gas in the wake of the war in Ukraine. Accordingly, Turkey’s aspirations to become an indispensable energy partner to Europe have been an important aspect of its foreign policy. “Our aim is to transform our country into a global center where the natural gas reference price is determined as soon as possible,” said Turkish President Recep Tayyip Erdogan at the inauguration of a natural gas storage facility in 2022. Nonetheless, a realistic assessment reveals Turkey’s lack of necessary resources to emerge as a genuine natural gas hub.

To function as a credible energy hub, a country must meet several key criteria. Some of these include substantial domestic production or long-term reliable access to diversified supply sources; sufficient infrastructure for storage, transit, and distribution; and politically and economically stable suppliers to sustain long-term energy investment.

At present, Turkey does not meet the basic requirements to establish an energy hub. Its domestic production is minimal, covering only a small fraction of national demand. The country relies heavily on imports. Furthermore, many of Turkey’s gas suppliers are politically unstable and weak, or embroiled in unresolved legal disputes over energy ownership and transit. Countries such as Iran and Russia have limited business partnership capabilities due to Western sanctions on their energy infrastructure and banking sector. Some prospective contributors, such as Iraq, face internal divisions and infrastructural bottlenecks that prevent them from delivering gas at scale. Egypt, once a potential LNG exporter, began importing gas again in 2024 due to surging domestic demand and declining production. Israel has significant offshore natural gas reserves. However, bilateral political relations between Turkey and Israel remain fragile.

While technical issues, regulatory frameworks, and market liberalization are among the principal elements of hub functionality, they are not within the scope of this analysis. This study focuses on the geopolitical dimensions and constraints shaping Turkey’s ambition to become a natural gas hub. The emphasis is on Turkey’s diplomatic relations with key supplier countries, the political instability across the wider Middle East, and the limited capacity of neighboring states to produce and export gas reliably—factors that collectively can make or undermine Turkey’s hub ambitions. However, in specific cases such as the Caspian Sea, international legal disputes that represent the most important obstacles will be briefly addressed.

Turkey’s natural gas reserves have expanded significantly in recent years, primarily due to major offshore discoveries in the Black Sea. The Sakarya gas field, discovered in 2020, holds an estimated 540 bcm of gas and began production in 2023. Turkey’s actual domestic output from this field averaged 9.5 million cubic meters (mcm) per day. If sustained throughout the year, this would amount to approximately 3.47 bcm annually. In May 2025, Turkey announced a new 75 bcm discovery at the nearby Göktepe-3 well.

Turkey’s annual natural gas consumption is approximately 60 bcm. Yet, in 2024, it met only 4% of its gas needs domestically and imported the rest. The government plans to increase domestic gas production to 7.5 bcm in the coming year. Even if the recently discovered reserves in the Black Sea reach their full potential, domestic output would still cover only an estimated 30 percent of the country’s total gas demand.

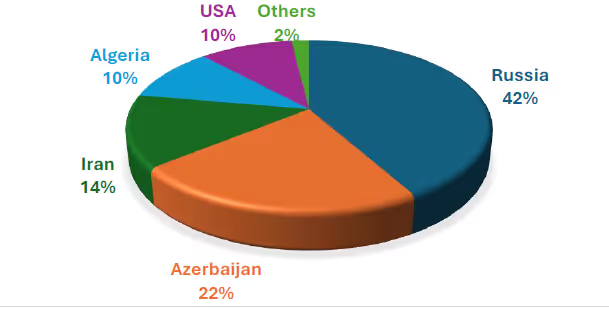

As domestic gas production is far from meeting demand, Turkey imported approximately 52 bcm of gas in 2024, based on the data provided by Turkey’s Energy Market Regulatory Authority (EPDK). Russia accounted for 42% of Turkey’s natural gas imports, followed by Azerbaijan with 22% and Iran with around 14%, while the remainder was supplied through LNG contracts from countries including Algeria (10.3%), the United States (10%), and others such as Egypt.

Figure 1 Turkey’s Natural Gas Imports by Country (2024, EPDK Data)

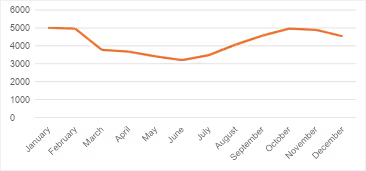

Turkey’s underground gas storage is incapable of supporting the balancing and arbitrage functions necessary for energy hubs. According to EPDK records, the average underground storage volume in 2024 was only 4.2 bcm, with the highest monthly level reaching 5 bcm in January, a fraction of the requirement for a functioning gas hub serving multiple regional markets.

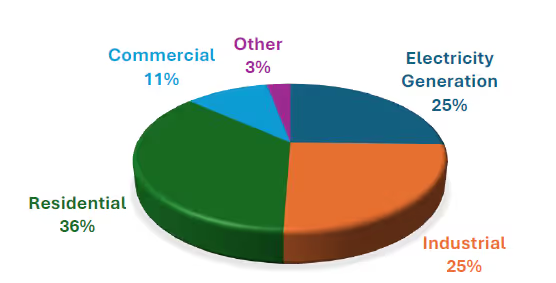

In 2024, natural gas accounted for approximately 18.5 percent of Turkey’s total electricity generation, according to a report by Ember. Coal's share in electricity fell from 36.9% to 35.6%, despite a 4 TWh rise in output. Hydropower contributed 22 percent, while renewable sources such as wind and solar provided 10.7 percent and 7.5 percent, respectively. These figures underscore the continued significance of natural gas in Turkey’s power sector.

On the other hand, Turkey’s energy demand is poised to dramatically increase. According to a forthcoming report by the Institute for Diplomacy and Economy (InstituDE), the country’s overall energy demand could double by 2050, placing additional strain on an already import-dependent system. As the transport sector shifts from petroleum to electricity, demand is expected to partially shift to the power sector, where natural gas remains a significant source of generation capacity.

In this context, Turkey may use more of its natural gas to meet growing domestic electricity demand. Without a significant and rapid expansion of renewable and nuclear capacity, natural gas will likely remain a key substitute for supplying electricity for peak loads and ensuring grid reliability. This shift will make it even harder for Turkey to accumulate surplus gas volumes for export or regional balancing—functions essential to any credible energy hub.

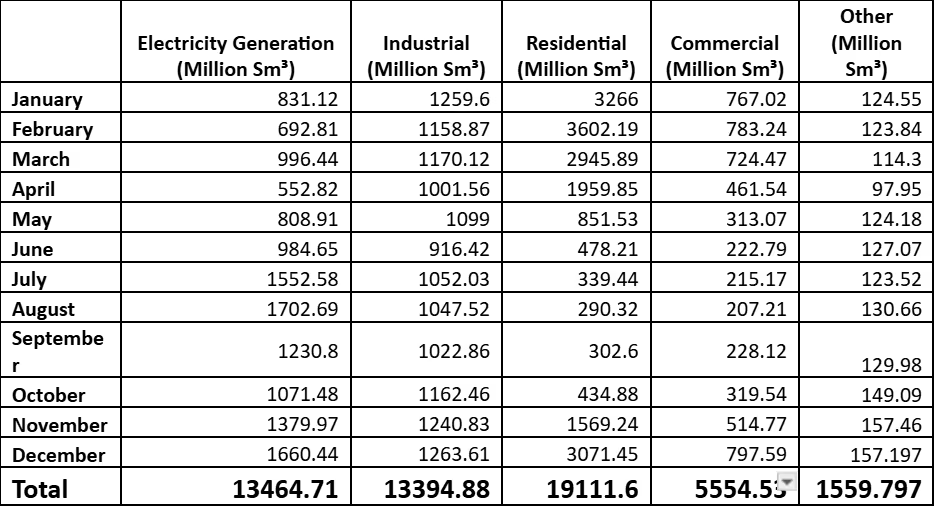

Figure 2 - Turkey's Natural Gas Consumption by Sector (2024, EPDK Data)

Insufficient production of domestic natural gas fundamentally limits Turkey’s ability to influence market dynamics. Due to its reliance on imports, the chances of Turkey becoming a hub hinge on a secure and reliable supply from other countries. Yet Turkey’s suppliers are unable or unwilling to supply gas in large quantities over a sustained period.

Russia is a prime candidate, with its vast natural gas reserves and extensive export infrastructure. With proven reserves of 47.8 trillion cubic meters (tcm) as of January 2024, it is the world's largest gas producer. A major share of Russian gas production was designated for export via major pipelines such as Nord Stream, Yamal-Europe, and Blue Stream, until the war in Ukraine. In 2023, Russia produced around 634 billion cubic meters of natural gas, with output rebounding to approximately 685 bcm in 2024. Its gas exports dropped to 142 bcm in 2023, from 244 bcm in 2021, amid European sanctions.

Russia currently exports gas to Turkey primarily through two pipelines: The Blue Stream pipeline, operational since 2003, carries up to 16 bcm annually via a direct undersea route across the Black Sea. The second is the TurkStream pipeline, inaugurated in 2020, with a total capacity of 31.5 bcm per year. Together, these pipelines provided the infrastructure for President Putin’s October 2022 proposal to establish a gas distribution hub in Turkey. The plan was enthusiastically endorsed by President Erdoğan, who viewed it as a way to elevate Turkey's geopolitical and energy stature.

Yet, the project was unsuccessful due to several fundamental reasons. First, Turkey’s westward export capacity to supply the EU through interconnectors between Greece and Bulgaria remains limited, making it difficult to scale up transit volumes. Most significantly, the EU’s commitment to phase out all Russian gas imports by 2027 in the wake of Russia’s invasion of Ukraine has rendered the project politically untenable. This lack of progress was highlighted in June 2025, when Russia’s Gazprom quietly shelved its plans to create a distribution hub in Turkey.

Figure 3 - Underground Gas Storage Levels in Turkey by Month (2024, EPDK Data, MMscm)

The federal government of Iraq is another potential supplier for Turkey with proven natural gas reserves of more than 3.5 tcm—the 12th largest in the world. Yet, it lacks the infrastructure to develop or export natural gas at scale. In 2023, Iraq produced more than 10 bcm of natural gas, which was consumed domestically. Total domestic gas consumption was 18.7 bcm. According to the Gas Market Report Q1-2025 of the International Energy Agency (IEA), Iraq has reduced gas flaring, yet it still captured only 65% of its gross natural gas output while flaring away 12 bcm annually. Besides, as Iraq struggles to meet its own domestic electricity demand, it imports gas and electricity from neighboring countries such as Iran and Turkey.

On the other hand, the semi-autonomous Kurdistan Regional Government (KRG) in northern Iraq has made separate efforts to position itself as an energy exporter. In 2025, the KRG signed a $110 billion agreement with US firms HKN Energy and WesternZagros to develop northern oil and gas fields. These fields—such as those in Dohuk and Erbil—are estimated to hold more than 200 bcm of gas, and the KRG has long sought to export to Turkey. However, Baghdad has declared the deal null and void, viewing it as a violation of Iraq’s constitutional provisions on federal control over natural resources.

This is not the first energy export disagreement between Baghdad and Erbil. In March 2023, Ankara suspended all oil exports from Iraq via the Kirkuk-Ceyhan pipeline following a ruling by the International Chamber of Commerce concerning its trade with the KRG without Baghdad’s consent. As of mid-2025, the pipeline remains closed, with Baghdad and Erbil unable to agree on revenue-sharing and operational terms. This disagreement also affects gas export plans, as any potential flows from the KRG would rely on a similar logistics and legal framework. This ongoing dispute between Erbil and Baghdad creates significant legal uncertainty for exporters and blocks energy export routes through Turkey.

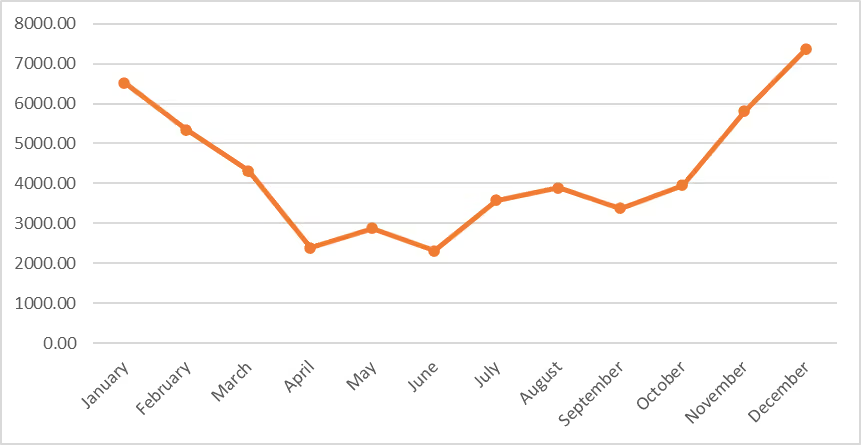

Figure 4 - Monthly Natural Gas Imports of Turkey (2024, EPDK Data, MMscm)

Iran possesses the world’s second-largest proven natural gas reserves, estimated at more than 34 tcm, second only to Russia. It is also the world’s third-largest dry gas producer, after the United States and Russia, with an annual output of 266 bcm as of 2023. Iran exports gas to Turkey via the Tabriz-Ankara pipeline, which has an annual capacity of 10 bcm. However, its potential as a stable and long-term gas supplier remains severely constrained by a combination of international sanctions, domestic needs, and chronic underinvestment in its energy infrastructure.

Firstly, Iran’s gas sector is largely cut off from international financing, technology transfers, and joint ventures due to Western sanctions, which have stalled both field development and pipeline modernization efforts. Secondly, a significant portion of Iran’s production is consumed internally, driven by rising demand in the residential, industrial, and power generation sectors. During periods of peak consumption, especially in winter, Tehran frequently prioritizes domestic use over exports. This pattern has resulted in recurring disruptions in gas exports to Turkey, which were officially attributed to technical issues. Lastly, the war between Iran and Israel, and the United States in June 2025, which partially halted gas production in some fields, showcased the instability in the region. Without a comprehensive political settlement with Western countries and the lifting of energy-related sanctions, Iran is unlikely to expand its export capacity or secure long-term contracts.

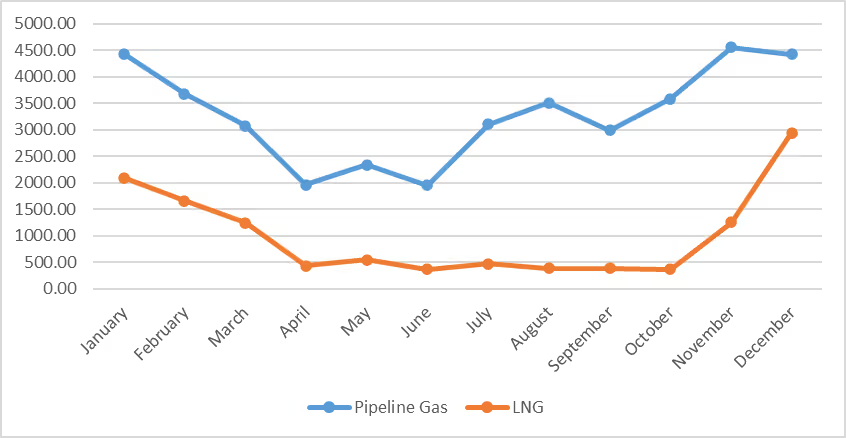

Figure 5 - Monthly LNG Vs. Pipeline Gas Imports of Turkey (2024, EPDK Data, MMscm)

Turkmenistan’s proven natural gas reserves are estimated at 11.3 tcm as of January 2025. Its natural gas production reached approximately 42 bcm in 2023, with the majority exported to China via the Central Asia-China gas pipeline. Ashgabat’s inability to diversify its export markets has left it dependent on a single large buyer and vulnerable to pricing pressure.

The long-discussed Trans-Caspian Gas Pipeline (TCP) may link Turkmenistan with Turkey and Europe. This proposed 300-kilometer subsea pipeline would connect Turkmenistan to Azerbaijan’s pipeline network, enabling onward delivery through the Southern Gas Corridor to Turkey and EU markets. Although the TCP is technically feasible and has received backing from the EU as a diversification measure, it remains stalled due to unresolved legal issues regarding seabed delimitation in the Caspian Sea. Both Russia and Iran have opposed the project, citing environmental concerns and legal ambiguity.

A gas swap agreement signed in 2025 between Turkey and Turkmenistan has provided a partial workaround. Under this arrangement, Turkmen gas is delivered to northeastern Iran, and an equivalent amount is supplied by Iran to Turkey. This allows limited Turkmen volumes to reach Turkey indirectly. Yet the swap relies entirely on Iranian infrastructure, which poses problems. Therefore, the swap mechanism is not a durable or scalable alternative to a dedicated export pipeline.

Figure 6 - Existing and Proposed Pipelines That Could Link Turkmenistan to Turkey

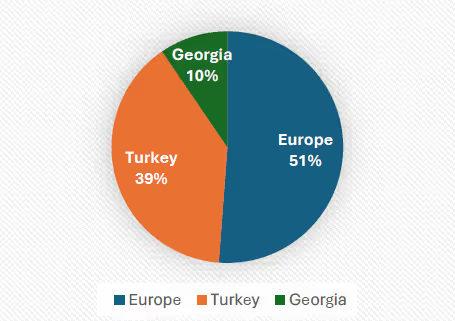

Azerbaijan, Turkey’s second-largest supplier, also presents notable limitations as a long-term contributor to Ankara’s hub ambitions. In 2024, Azerbaijan’s total natural gas exports grew by 5.8% in 2024 to 25.2 bcm. Europe was the primary destination for Azerbaijani gas, importing 12.9 bcm, accounting for approximately 51% of total exports in 2024. Georgia received the smallest share, with 2.4 bcm, about 10% of Azerbaijan’s gas exports. In 2024, Azerbaijan supplied more than 10 bcm of natural gas to Turkey.

However, Azerbaijan’s production capacity is expected to plateau in the coming years. According to official budget projections, commercial gas output is set to decline from 38.4 bcm in 2025 to 36.6 bcm by 2028. Besides, as Azerbaijan uses more gas at home to generate electricity, it becomes harder to have surplus gas available for export.

Figure 7 - Azerbaijan Gas Exports by Destination (2024, Total 25.2 bcm)

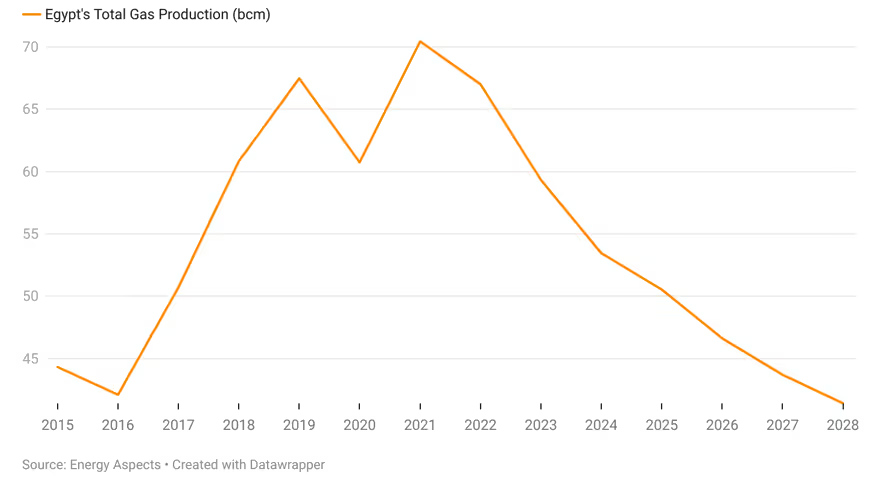

Egypt holds proven natural gas reserves of around 2.2 tcm. According to the Joint Organizations Data Initiative (JODI), Egypt’s natural gas production fell by 16.7% in 2024 to 49.4 bcm, from 59.3 bcm in 2023. This downward trend is expected to continue due to natural field depletion, delayed investment, and a lack of new oil discoveries. At the same time, its domestic gas consumption increased to 62.5 bcm, driven by rapid population growth, industrial expansion, and increased electricity demand. Natural gas accounts for more than 80% of Egypt’s power generation.

Egypt, once viewed as a promising LNG exporter in the Eastern Mediterranean, has now become a net importer. To mitigate electricity shortages, particularly during peak summer months, Egypt began LNG imports in 2024 for the first time since 2018. It now imports 15–20 percent of its gas consumption from Israel. Cairo has also been seeking long-term LNG import contracts through 2030, including from suppliers in the Gulf and European traders. Egypt’s increasing gas demand effectively disqualify it as a reliable contributor to Turkey’s hub aspirations.

Figure 8 - Egypt's Total Gas Production (bcm)

Source: Reuters

Israel possesses substantial offshore natural gas reserves, with total proven resources estimated at 1087 bcm at the end of 2022. Production has grown steadily, reaching 27 bcm in 2024, and is expected to rise 4% in 2025 to approximately 28 bcm as field development continues. These reserves offer potential for regional exports via LNG or pipeline, and Israel has signed export agreements with Egypt and Jordan. It also plans to connect to Europe via the long-discussed EastMed pipeline, which will be challenging.

On the other hand, the prospect of routing Israeli gas through Turkey—either directly or as part of a broader regional export scheme—remains highly uncertain due to enduring problems in bilateral relations. Ankara and Tel Aviv have periodically downgraded and restored diplomatic ties since 2010. Turkey halted official trade with Israel in 2024, following public pressure over Israel’s military operations in Gaza. In addition, Ankara formally joined the genocide case brought against Israel at the International Court of Justice in 2025. In return, Israeli officials have repeatedly criticized President Erdoğan as a dictator. “Erdogan is breaking agreements by blocking ports for Israeli imports and exports. This is how a dictator behaves. I have instructed to create alternatives for trade with Turkey,” Israeli Foreign Minister Israel Katz posted on X.

The Turkish-Israeli relationship remains deeply vulnerable to other regional developments, such as their diverging views on the new Syrian government. This hostile diplomatic environment between Turkey and Israel creates a high-risk context for energy investors, who are unlikely to commit to multi-billion-dollar infrastructure projects under these circumstances. This is why proposals for a pipeline connecting Israel’s gas fields to Turkey’s southern coast have stalled.

Turkey’s most realistic path over the coming decades may lie in enhancing its domestic energy resilience. Structural challenges such as limited domestic production, unstable and often sanctioned suppliers, and insufficient westward infrastructure constrain its energy hub ambitions. Nonetheless, the energy hub project is, by its nature, a long-term endeavor. If Turkey undertakes necessary reforms and investments, and addresses key structural gaps, this potential could still be realized to some extent in the coming decades.

Regarding domestic resources, Turkey could strengthen its position by tapping into shale gas. This will require sustained investment in exploration, technology transfer, and regulatory reforms. Similarly, recent offshore discoveries in the Black Sea, if developed at scale, could bolster the supply and reduce reliance on imports.

On the infrastructure front, Turkey must accelerate efforts to expand LNG regasification capacity and underground storage. This would support domestic resilience as well as allow for more flexible participation in regional and global markets, especially as LNG trade plays an increasingly central role in the international gas economy.

Equally important will be Turkey’s ability to repair and enhance its regional diplomacy. Improved ties with neighboring countries could open doors to new supply routes, joint infrastructure projects, and more reliable regional partnerships. The erosion of Turkey’s relations with the EU, Israel, and several neighbors over the past decade has limited its options and, at times, excluded it from energy projects that bypass its territory, such as the India-Middle East-Europe Economic Corridor (IMEC) and EastMed pipeline.

Finally, no technical or diplomatic initiative can succeed without a stable political framework at home. Turkey needs a consistent energy strategy. Upholding the rule of law and honoring its commitments will be decisive.

Turkey’s ambition to become a regional natural gas hub offers political appeal, promising economic gains as well as geopolitical leverage. Yet, its current supply limitations and exposure to regional geopolitical instability tell a different story. Unless these structural constraints are addressed, the vision of Turkey as a natural gas hub remains, for now, largely aspirational.

Appendix

Table 1- Turkey’s Natural Gas Imports by Country (2024, EPDK Data, MMscm)

Table 2 Turkey's Natural Gas Consumption by Sector (2024, EPDK Data, MMscm)

Mustafa Kamaci, “Türkiye Eyes Becoming Global Hub for Setting Price of Natural Gas, Says President Erdogan,” Anadolu Agency, December 16, 2022, https://www.aa.com.tr/en/economy/turkiye-eyes-becoming-global-hub-for-setting-price-of-natural-gas-says-president-erdogan/2765740.

Mahmoud A. Hammad, Sara Elgazzar, Borut Jereb, and Marjan Sternad, Requirements for Establishing Energy Hubs: Practical Perspective, Amfiteatru Economic 25, no. 64 (2023): 798–812, https://doi.org/10.24818/EA/2023/64/798.

“Sakarya Gas Field Development, Black Sea, Turkey,” Offshore Technology, February 1, 2023, https://www.offshore-technology.com/projects/sakarya-gas-field-development-black-sea-turkey/.

Nevzat Devranoglu, “Turkey Eyes Regional Energy Expansion as Black Sea Gas Output Rises,” Reuters, April 21, 2025, https://www.reuters.com/business/energy/turkey-eyes-regional-energy-expansion-black-sea-gas-output-rises-2025-04-21/.

“Turkey Finds New Natural Gas Reserve in Black Sea, Erdogan Says,” Reuters, May 17, 2025, https://www.reuters.com/business/energy/turkey-discovers-new-75-bcm-natural-gas-reserve-black-sea-erdogan-says-2025-05-17/.

Ufuk Alparslan, “Türkiye Electricity Review 2025,” Ember, April 10, 2025. https://ember-energy.org/app/uploads/2025/03/Turkiye-Electricity-Review-2025_11032025.pdf

“Türkiye Hikes Gas Output from Vast Black Sea Reserve to 8.8 Mcm,” Daily Sabah, April 11, 2025, https://www.dailysabah.com/business/energy/turkiye-hikes-gas-output-from-vast-black-sea-reserve-to-88-mcm.

“Türkiye Launches Black Sea Gas Deliveries in Historic Milestone,” Daily Sabah, April 20, 2023, https://www.dailysabah.com/business/energy/turkiye-launches-black-sea-gas-deliveries-in-historic-milestone.

“Doğal Gaz Piyasası Aylık Sektör Raporu Listesi,” T.C. Enerji Piyasası Düzenleme Kurumu (EPDK), https://www.epdk.gov.tr/Detay/Icerik/3-0-95-1007/dogal-gazaylik-sektor-raporu.

Türkiye Sınai Kalkınma Bankası (TSKB), Enerji Görünümü 2024, https://www.tskb.com.tr/uploads/file/enerji-gorunumu-2024.pdf

EPDK, “Doğal Gaz Piyasası Aylık Sektör Raporu Listesi.

Alparslan, “Türkiye Electricity Review 2025.”

“Russia: Country Analysis Brief,” U.S. Energy Information Administration (EIA), April 29, 2024, https://www.eia.gov/international/content/analysis/countries_long/Russia/pdf/russia.pdf .

“Gazprom’s Production Will Exceed 400 Bln Cubic Meters in 2024, Russian Production 690 Bln Cubic Meters,” Interfax, December 11, 2024, https://interfax.com/newsroom/top-stories/108464/.

“Gas Production in Russia Rises 7.6% in 2024 to around 685 Bcm - Novak,” Interfax, January 30, 2025, https://interfax.com/newsroom/top-stories/109480/.

Anne-Sophie Corbeau and Tatiana Mitrova, “Russia’s Gas Export Strategy: Adapting to the New Reality,” Center on Global Energy Policy at Columbia University SIPA, February 21, 2024, https://www.energypolicy.columbia.edu/publications/russias-gas-export-strategy-adapting-to-the-new-reality/.

Prasanta Kumar Dutta, Samuel Granados, and Michael Ovaska, “The Ukraine Crisis and Russia’s Gas Threat in Europe,” February 21, 2022, https://www.reuters.com/graphics/UKRAINE-CRISIS/GAS/gdpzynlxovw/.

“Putin Courts Erdogan with Plan to Pump More Russian Gas via Turkey,” Reuters, October 13, 2022, https://www.reuters.com/world/europe/putin-puts-gas-hub-plan-turkeys-erdogan-2022-10-13/.

“Erdogan Says He Agreed with Putin to Form Natural Gas Hub in Turkey,” Reuters, October 19, 2022, https://www.reuters.com/business/energy/erdogan-says-he-agreed-with-putin-form-natural-gas-hub-turkey-2022-10-19/.

Kate Abnett and Lili Bayer, “EU to Propose End-2027 Halt to All Russian Gas Imports,” Reuters, May 6, 2025, https://www.reuters.com/sustainability/climate-energy/eu-set-out-plan-phasing-out-final-russian-gas-supplies-2025-05-06/.

“Gazprom Abandons Idea of Turkish Backdoor to Europe’s Gas Market,” Bloomberg, June 3, 2025, https://www.bloomberg.com/news/articles/2025-06-03/russia-abandons-idea-of-turkish-backdoor-to-europe-s-gas-market.

“Iraq,” U.S. Energy Information Administration (EIA), February 14, 2024, https://www.eia.gov/international/analysis/country/irq.

“BP Finalises Contract to Redevelop Oil Fields in Iraq with a 20 Gboe Potential,” Enerdata, March 28, 2025, https://www.enerdata.net/publications/daily-energy-news/bp-finalises-contract-redevelop-oil-fields-iraq-20-gboe-potential.html.

“Enabling Iraq’s Energy Independence,” Petroleum Economist, November 28, 2024, https://pemedianetwork.com/petroleum-economist/articles/gas-lng/2024/enabling-iraq-s-energy-independence.

International Energy Agency (IEA), Gas Market Report, Q1-2025, March 2025, https://iea.blob.core.windows.net/assets/6bd6c46d-21d7-4ae7-af9f-25dc9f8e7f3b/GasMarketReport%2CQ1-2025.pdf .

Robin Mills, “Iraq Must Act Fast to Avoid a Domestic Energy Crisis,” AGBI, February 18, 2025, https://www.agbi.com/opinion/energy/2025/02/iraq-must-act-fast-to-avoid-a-domestic-energy-crisis/.

“The End of a Waiver: Iraq’s Struggle for Energy Independence,” Shafaq News, March 12, 2025, https://shafaq.com/en/Report/The-end-of-a-waiver-Iraq-s-struggle-for-energy-independence.

“US Backs More Energy Investment in Kurdistan Region: Energy Secretary e since 2012,” Al-Monitor, May 22, 2025, https://www.al-monitor.com/originals/2025/05/us-backs-more-energy-investment-kurdistan-region-energy-secretary.

“US Energy Firms’ Deals with Iraqi Kurdistan ‘Null and Void’, Baghdad Says,” Reuters, https://www.reuters.com/business/energy/us-energy-firm-deals-with-iraqi-kurdistan-null-void-baghdad-says-2025-05-20/.

Ahmed Rasheed and Rowena Edwards, “Iraq Halts Northern Crude Exports after Winning Arbitration Case against Turkey,” Reuters, March 25, 2023,https://www.reuters.com/business/energy/iraq-halts-northern-crude-exports-after-winning-arbitration-case-against-turkey-2023-03-25/.

Mustafa Enes Esen, “KRG’s Energy Deals Will Likely Proceed Without a Turkish Route,” Institute for Diplomacy and Economy, May 23, 2025, https://www.institude.org/opinion/krgs-energy-deals-will-likely-proceed-without-a-turkish-route.

“Iran,” U.S. Energy Information Administration (EIA), October 10, 2024, https://www.eia.gov/international/analysis/country/irn.

“Iran.”.

“Turkey Orders Cuts to Gas Use as Flow Halted from Iran,” Reuters, January 20, 2022, https://www.reuters.com/world/middle-east/iran-gas-flow-turkey-cut-by-technical-failure-officials-2022-01-20/.

“Iran Says Production at World’s Largest Gas Field Partly Suspended after Israeli Attack,” Reuters, June 14, 2025, https://www.reuters.com/world/middle-east/iran-says-production-worlds-largest-gas-field-partly-suspended-after-israeli-2025-06-14/.

“Caspian Sea Regional Analysis Brief 2025,” U.S. Energy Information Administration (EIA), February 6, 2025, https://www.eia.gov/international/content/analysis/regions_of_interest/Caspian_Sea/pdf/Caspian%20Sea%20Regional%20Analysis%20Brief%202025.pdf .

“Caspian Sea Regional Analysis Brief 2025.”.

Mustafa Enes Esen, “Would Turkmen Gas Make Turkey an Energy Hub?,” Institute for Diplomacy and Economy, December 19, 2022, https://www.institude.org/opinion/would-turkmen-gas-make-turkey-an-energy-hub.

“The Convention on the Legal Status of the Caspian Sea - A Sea or Not a Sea: That Is Still the Question,” Norton Rose Fulbright, September 2018, https://www.nortonrosefulbright.com/en/knowledge/publications/5f222b95/the-convention-on-the-legal-status-of-the-caspian-sea---a-sea-or-not-a-sea-that-is-still-the-question.

Mustafa Enes Esen, “Turkey-Turkmenistan Gas Deal: A Strong Start, but Its Full Potential Remains Uncertain,” Institute for Diplomacy and Economy, February 14, 2025, https://www.institude.org/opinion/turkey-turkmenistan-gas-deal-a-strong-start-but-its-full-potential-remains-uncertain.

Parviz Shahbazov (@ParvizShahbazov), Twitter (now X), January 15, 2025, https://x.com/ParvizShahbazov/status/1879397594805551481.

“Oil and Gas Production in Azerbaijan to Gradually Decline in 2025-2028,” Azeri-Press Agency (APA), November 18, 2024, https://en.apa.az/energy-and-industry/oil-and-gas-production-in-azerbaijan-to-gradually-decline-in-2025-2028-453638.

“Azerbaijan’s Gas Exports to the EU Face Challenges,” Economist Intelligence Unit, July 10, 2023, https://www.eiu.com/n/azerbaijans-gas-exports-to-the-eu-face-challenges/.

“Egypt Announces Discovery of a Gas Field with 99 Bcm of Estimated Reserves,” Enerdata, December 19, 2022, https://www.enerdata.net/publications/daily-energy-news/egypt-gas-reserve-discovery.html.

“Egypt to Receive 4 Liquefied Natural Gas Shipments in April 2024,” Business Today, March 13, 2025, https://www.businesstodayegypt.com/Article/1/6140/Egypt-to-receive-4-liquefied-natural-gas-shipments-in-April.

“Egypt to Receive 4 Liquefied Natural Gas Shipments in April 2024.”.

“Egypt,” Ember, April 11, 2025, https://ember-energy.org/countries-and-regions/egypt/#data.

Marwa Rashad et al., “Exclusive: Egypt Counts on Foreign Funds to Buy Gas as Power Crisis Worsens,” Reuters, September 2, 2024, https://www.reuters.com/business/energy/egypt-counts-foreign-funds-buy-gas-power-crisis-worsens-2024-09-02/.

Steven Scheer and Mohamed Ezz, “Israel’s Gas Fields Resume Operations after Shutdown during Iran Conflict,” Reuters, June 25, 2025, https://www.reuters.com/business/energy/israels-leviathan-natural-gas-field-resume-operations-few-hours-2025-06-25/.

Marwa Rashad, “Egypt Agrees to Buy up to 160 LNG Cargoes through 2026, Sources Say,” Reuters, June 12, 2025, https://www.reuters.com/sustainability/boards-policy-regulation/egypt-agrees-buy-up-160-lng-cargoes-through-2026-sources-say-2025-06-12/.

Basel Mahmoud, “How Egypt Is Managing Energy Deficit in a Sweltering Summer? - Energy - Business,” Ahram Online, June 6, 2025, https://english.ahram.org.eg/NewsContent/3/16/547535/Business/Energy/How-Egypt-is-managing-energy-deficit-in-a-swelteri.aspx.

“Israel’s Gas Reserves Grew by 40% over Past Decade, Report Says,” Reuters, June 22, 2023, https://www.reuters.com/business/energy/israels-gas-reserves-grew-by-40-over-past-decade-report-2023-06-22/.

Gas Market Report, Q1-2025, IEA, https://www.iea.org/reports/gas-market-report-q1-2025.

Mustafa Enes Esen, “Unfreezing the Relations: Turkey and Israel,” Institute for Diplomacy and Economy, March 11, 2022, https://www.institude.org/opinion/unfreezing-the-relations-turkey-and-israel.

Turkey Halts All Trade with Israel, Cites Worsening Palestinian Situation,” Reuters, May 2, 2024, https://www.reuters.com/world/middle-east/israel-says-turkeys-erdogan-is-breaking-agreements-by-blocking-ports-trade-2024-05-02/.

“Application of the Convention on the Prevention and Punishment of the Crime of Genocide in the Gaza Strip ((South Africa v. Israel),” International Court of Justice, April 14, 2025, https://www.icj-cij.org/case/192.

Israel Katz (@Israel_katz), tweet, Twitter (now X), May 2, 2024, https://x.com/Israel_katz/status/1786047725332492589.

Mustafa Enes Esen, “Containment vs. Consolidation: Israel and Turkey’s Diverging Visions on Syria,” Institute for Diplomacy and Economy, April 9, 2025, https://www.institude.org/opinion/containment-vs-consolidation-israel-and-turkeys-diverging-visions-on-syria.

Haşim Tekineş, “Shifting Geopolitics of Turkey-Israel Relations After Assad,” Institute for Diplomacy and Economy, December 20, 2024, https://www.institude.org/opinion/shifting-geopolitics-of-turkey-israel-relations-after-assad.