After beginning its second term in January 2025, US President Trump embraced a trade policy centered on imposing high tariffs at unprecedented levels on almost all countries, with China facing some of the most severe measures.1 In an attempt to counter these unprecedented US tariffs, China retaliated with similar trade measures and restricted the exports of its rare earth elements (REEs) to the US.2 Given that REEs underpin everything from electric vehicle motors and wind turbine generators to precision-guided munitions and fighter aircraft,3 the restrictions sent shockwaves through global supply chains, disrupting factory production.4 For Western governments and manufacturers alike, it was a stark reminder of how dependent critical industries remain on a single supplier. As trade tensions escalated, strategic dependencies within critical mineral supply chains became an increasingly urgent concern for Washington. US President Trump, therefore, persistently sought to secure access to rare earth reserves abroad, from Ukraine and the Democratic Republic of Congo to Greenland.5

In this context, Turkey's reported rare earth reserves came to the fore, raising hopes in Ankara about whether the country could emerge as a meaningful alternative to Chinese supply. Turkey’s engagement with REEs dates to 2022, when Turkey announced the discovery of approximately 694 million tons of REE ore at Beylikova.6 If confirmed, the deposit would constitute the world's second-largest known concentration of REEs after China's Bayan Obo mine in Inner Mongolia.

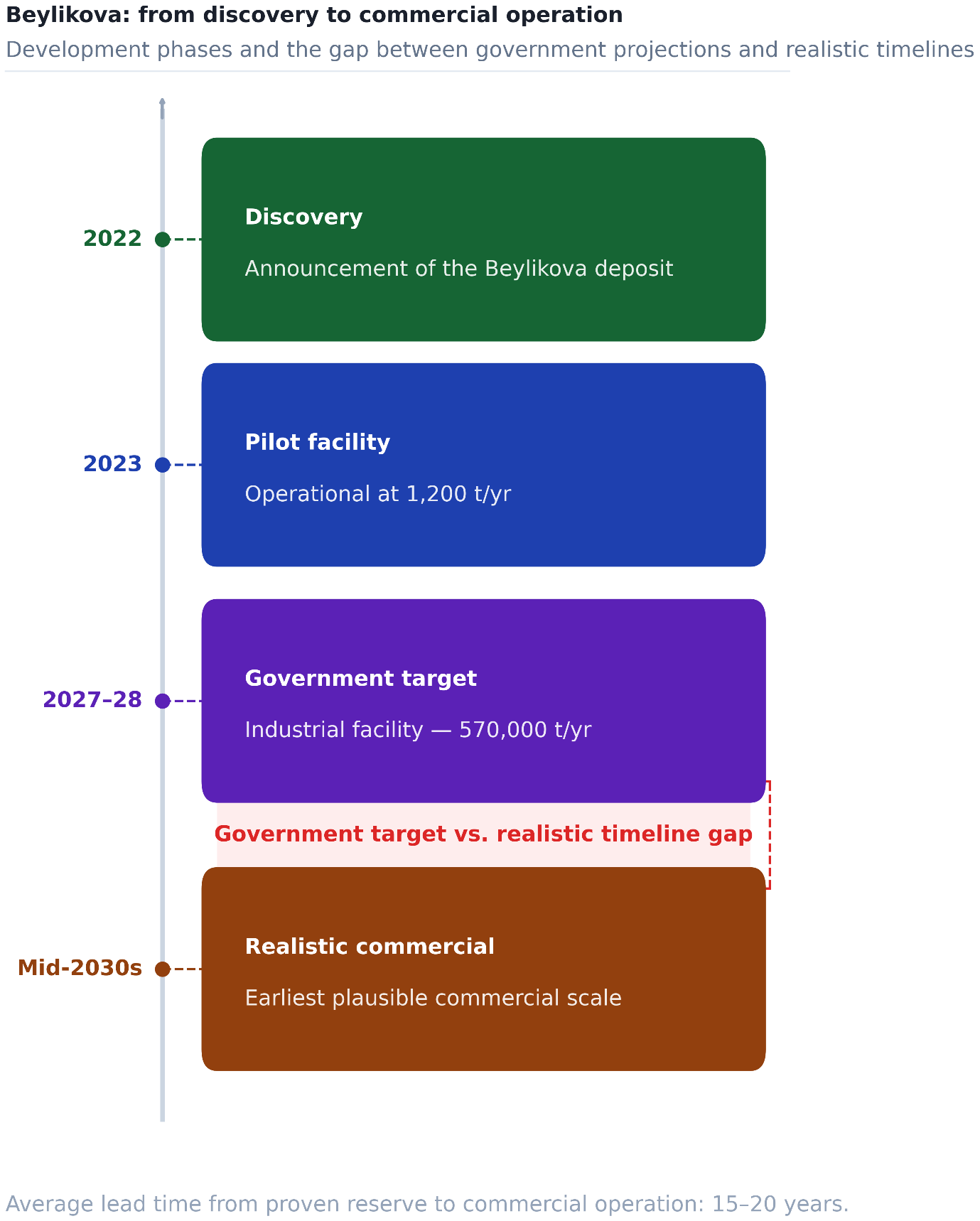

The subsequent years have translated that initial announcement into a concrete, if still early-stage, development program. Eti Maden, the wholly state-owned mining enterprise, established a pilot processing facility at Beylikova, inaugurated in late 2023 with a capacity of 1,200 tons of ore per year.7 The Turkish government has outlined a three-phase development roadmap: a pilot facility currently operational at 1,200 tons per year, scaling to 500,000 tons annually in a second phase projected for 2028-2032, with full global positioning targeted by 2035.8 However, these projections remain contingent on successful reserve verification, financing, and processing scale-up.

While delays and downward revisions are not uncommon in major extractive projects globally, Turkey’s recent experience has heightened skepticism regarding official projections. Turkey has a documented pattern of announcing major natural resource discoveries with considerable political fanfare, only for the subsequent development trajectory to fall short of the initial claims. The Black Sea natural gas discovery at the Sakarya field, announced by President Erdoğan in 2020 with projections of energy independence, has proceeded far more slowly than official timelines suggested and has yet to deliver the transformative impact on Turkey's energy import bill that was promised.9 Whether the REEs in Beylikova will face the same fate remains to be seen.

This report is addressed to two audiences simultaneously: Turkish policymakers weighing how to develop the Beylikova deposit, and Western governments and companies assessing whether Turkey is a credible partner in their supply chain diversification strategies. It examines both the opportunities Turkey’s entry into the rare earth sector could realistically generate and the structural obstacles that stand between the current situation and those outcomes.

The obstacles facing Turkey are numerous and structural. The 694 million-ton figure remains unverified under international standards, China retains overwhelming dominance in refining capacity, and the environmental and institutional challenges associated with radioactive byproducts remain substantial. The opportunities, however, are real. Western governments have committed substantial public financing to non-Chinese rare earth supply chains, and the Beylikova ore aligns with the highest-value commercial applications. Whether Turkey can overcome these challenges and seize the moment remains an open question.

In 2023, Lütfi Tozar, Director of the Beylikova Fluorite, Barite, and REE Operation, stated that the deposit in Beylikova contains seven REEs at commercially producible levels: lanthanum, cerium, praseodymium, samarium, gadolinium, europium, and neodymium.10 Tozar added that the remaining REEs are also present at the site in certain proportions, and that thorium will likewise be processed at the facility. Thorium is a nuclear fuel raw material and not an REE, a distinction with significant implications for waste management that is discussed in the Environmental Risks section of this report. In October 2025, President Erdoğan stated that 10 of the 17 known REEs are present at Beylikova, with approximately 12.5 million tons of rare earth oxides identified.11 The Beylikova deposit presents Turkey with a set of challenges that are simultaneously technical, institutional, and geopolitical. This section examines each in turn.

The most immediate challenge Turkey faces is one of credibility. The Mineral Research and Exploration General Directorate (MTA) of Turkey was, for many decades, the principal body responsible for geological surveying and reserve classification.12 A legislative change around 2005, however, transferred MTA's accumulated reserve data to private entities and restricted public access to geological information.13 Mining professionals note that research databases once available to academics and investors now require substantial fees to access, reducing the transparency of the information environment on which investment decisions depend.14

Since MTA's reserve data was transferred to private control, independent scientific assessment of Turkey's mineral base has become structurally more difficult. The Ministry of Energy's 2025 Strategic Critical Minerals Report15 — the primary official document on Turkey's mineral sector ambitions — has been criticized by mining engineers for drawing exclusively on ministerial data and defense industry sources, without engagement with academic specialists, engineering professional bodies, or independent practitioners.16

The widely cited figure of 694 million tons, used to support Turkey’s claim of holding the world’s second-largest rare earth reserves, is, in fact, a resource estimate rather than a proven reserve. This distinction is critical. A resource estimate reflects the quantity of material identified through preliminary geological surveys and drilling. By contrast, a proven reserve represents the portion of that resource that has been rigorously verified as economically and technically viable to extract under defined legal and market conditions. It is this latter classification that underpins investor confidence, determines whether projects can secure financing, and is recognized in official international reserve rankings.

The data from Beylikova has not yet been certified under any internationally recognized reporting standard — such as the Joint Ore Reserves Committee (JORC) code, which is widely used as the global benchmark for classifying mineral reserves and is relied on by most major mining investors.17 JORC certification requires independent geological verification, full transparency around drilling data, and lab-confirmed analysis of ore grades. In practice, that level of disclosure and external validation requires a degree of institutional transparency that observers argue has not always characterized Turkey’s mining sector governance.

Yalcin Aydin, chairman of Eti Maden, states that Turkey has applied for JORC or equivalent international certification for the Beylikova deposit, although the process remains incomplete.18 Because of that, Turkey’s deposit does not appear in authoritative listings such as the United States Geological Survey’s Mineral Commodity Summaries, where global rare earth reserve rankings are formally tracked.19

On the other hand, early political messaging complicated the issue by blurring the line between total ore tonnage and the actual concentration of rare earth oxides within that ore—a distinction that is crucial in mining economics.20 Independent assessments were quick to point out that the headline figures referred to the overall volume of material in the ground, not the portion that can realistically yield commercially valuable REEs.

Lower ore grades significantly increase extraction and processing costs, reducing the economic attractiveness of large-scale commercial production. Kathryn Goodenough, Chief Geologist at the British Geological Survey, has cautioned against describing the Beylikova discovery as a major new reserve in the absence of a formal assessment against international industry standards.21 Without that level of verification, she notes, it remains unclear how much of the deposit is actually recoverable.22

The uncertainty is not merely procedural. Current modeling assumes a total rare earth oxide (TREO) grade of approximately 1.75% across the 694 million-ton resource.23 This would yield approximately 12.5 million tons of rare earth oxide potential and place Turkey third globally after China and Brazil.24 Under more conservative grade assumptions of around 1% TREO, however — which some independent geologists consider more realistic — Turkey's ranking would fall to the fourth-to-sixth range globally, with a correspondingly lower economic recovery rate.25

As a mining expert explained to the Institute for Diplomacy and Economy, Turkey’s domestic track record in developing critical minerals should also be closely examined to better assess the country’s rare earth mineral prospects. The country holds roughly 73% of the world’s known boron reserves and has mined boron for decades, yet it has struggled to build a commercially significant, value-added downstream industry.26 In this regard, the trajectory of BOREN, the National Boron Research Institute, is frequently cited as a cautionary parallel: established with substantial expectations, it has produced limited commercially scalable industrial applications relative to Turkey's boron reserve endowment.27 Similarly, despite a long history of gold extraction, Turkey has not established a robust domestic refining base. The Turkish Miners Association has acknowledged this broader pattern, warning that the country exports its minerals mainly in raw form and that shifting toward value-added processing could add billions of dollars annually to export revenues.28

The rare earth sector is considerably more complex than either of these. Making a credible case for success will require more than pointing to the scale of a deposit. It depends on demonstrating real progress in processing technology, building institutional and technical capacity, and strengthening governance frameworks—areas where Turkey’s past performance in industrial scaling and institutional coordination has been uneven.

A fundamental characteristic of rare earth mining complicates the risk picture further: the ratio of usable material to total ore processed is extremely low. REE ore rarely occurs in economically concentrated form, meaning that large-scale excavation and extensive chemical processing are required to isolate commercially viable quantities. Scientific assessments indicate that producing one ton of rare earth oxides can generate thousands of tons of tailings — waste material typically containing toxic heavy metals, processing acids, and radioactive residues.29 These tailings pose long-term risks that are particularly serious in regions lacking established regulatory oversight and technical expertise in radioactive waste handling, areas in which Turkey currently has limited institutional experience.

The most environmentally damaging phase is not mining itself but chemical processing. Separating individual REEs requires repeated solvent extraction steps using strong acids, organic solvents, and complexing agents.30 These processes produce acidic wastewater, toxic sludge, and airborne emissions that are difficult and expensive to control. Each ton of rare earth oxide produced generates approximately 13 kilograms of particulate dust, between 9,600 and 12,000 cubic meters of waste gas, 75 cubic meters of wastewater, and one ton of radioactive processing residue.31 Even among the world's largest and most reputable mining companies, including members of the International Council on Mining and Metals, one-third of tailings facilities had not achieved full conformance with the Global Industry Standard on Tailings Management as of 2025.32 This indicates that adequate waste management remains a work in progress even in the most experienced jurisdictions. The Beylikova site's proximity to agricultural land intensifies these concerns considerably: contaminated runoff from a nearby processing facility could render both soil and water sources unusable for decades.33

The history of how Western countries dealt with these costs is instructive, and directly relevant to the choices Turkey now faces. Starting in the late twentieth century, increasingly stringent environmental regulations in Europe and North America raised the cost of rare earth processing to the point where domestic operations became uncompetitive.34 Western companies responded by gradually outsourcing processing to China, where environmental standards were less strictly enforced. This strategic shift effectively transferred the environmental burden from consumer countries to producer regions.

What followed in China was extensive ecological degradation, including contaminated rivers, uninhabitable farmland, and elevated cancer rates in mining communities.35 China's Bayan Obo mine generates over 70,000 tons of radioactive waste annually, and despite regulatory interventions since 2012, satellite imagery and independent field reporting continue to document arsenic and heavy metal contamination of agricultural land and groundwater in its vicinity.36 In Myanmar, where heavy rare earth extraction has expanded rapidly with Chinese investment, environmental controls have been largely absent, with severe consequences for local ecosystems and communities.37 Contamination documented in rare earth mining regions has, in some cases, been detected dozens of kilometers downstream from processing facilities, affecting water sources and agricultural land far removed from the mine itself.38

Preventing this level of damage requires substantial capital investment from the outset. Advanced tailings storage facilities, wastewater treatment infrastructure capable of handling acidic and radioactive effluents, continuous environmental monitoring systems, and worker radiation protection measures are not optional add-ons but structural prerequisites for responsible operation. These investments significantly increase both capital expenditure and ongoing operating costs, reducing competitiveness against producers operating under looser standards.

The lesson is not that environmental protection is impossible in rare earth production, but that it is expensive, and that the temptation to defer or avoid those costs produces consequences that are severe, long-lasting, and ultimately politically costly. For Turkey, which would be entering the sector with no existing environmental infrastructure calibrated to radioactive waste from mining, these upfront costs would be substantial. Embedding them from the beginning of the project lifecycle is both more effective and ultimately less costly than attempting remediation after damage has occurred — as China's experience, and the continued expense of managing its legacy contamination, demonstrates clearly.39

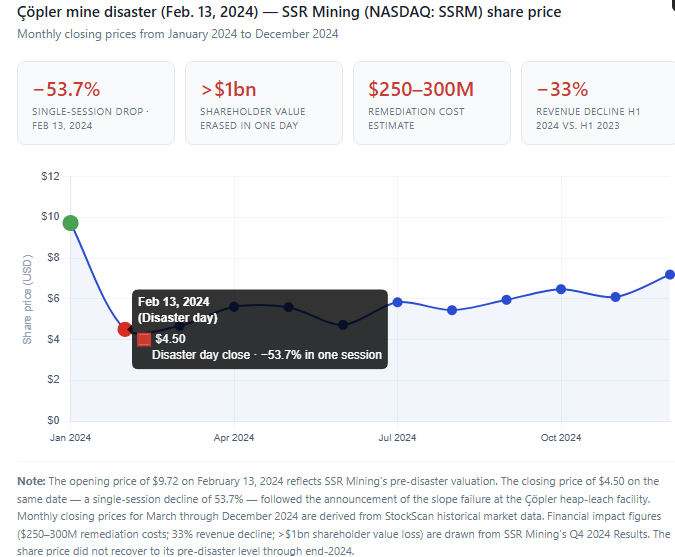

The regulatory record in Turkey’s broader mining sector raises additional concerns. The February 2024 slope failure at the Çöpler gold mine in İliç, Erzincan, which killed nine workers when a heap-leach pad containing cyanide-saturated ore collapsed, is the most recent and consequential illustration of what occurs when regulatory oversight fails to match industrial ambition.40 On February 13, 2024, SSR Mining (NASDAQ: SSRM), the Denver-based company that cooperated the Çöpler gold mine through its Turkish subsidiary Anagold, saw its share price fall 53.7% in a single trading session — closing at $4.50 after opening at $9.72, erasing more than $1 billion in shareholder value in one day.41 The stock had not recovered to its pre-disaster level months later, and the company faced a securities fraud class action lawsuit alleging it had misled investors about its safety practices. Remediation costs were estimated at $250–$300 million, according to SSR Mining Inc.42 Revenues declined by roughly one-third year-over-year in the first half of 2024, while gold production at Çöpler collapsed following the suspension of operations at the site.43

According to an independent geological assessment, the collapse was foreseeable and preventable: warning signals, including measurable ground movements of 25 millimeters per day in January 2024, had been visible for months and were either dismissed or disregarded by both the operating company and the relevant inspectorates.44 The disaster unfolded amid broader concerns regarding the consistency of regulatory oversight in the mining sector. In June 2022, mining activities at the Çöpler site were temporarily suspended after a diluted cyanide solution spilled from a pipeline on the heap-leach pad, leading to intervention by the relevant environmental authorities.45 While the company and the authorities maintained that the spill had not reached the Euphrates, environmental groups challenged the adequacy of the official response, as an expert explained to the Institute for Diplomacy and Economy.

Of the 1,368 mining project applications submitted in Turkey in 2024, 1,153 were exempted from comprehensive environmental impact assessment reviews.46 This pattern of regulatory accommodation is directly relevant to assessing Turkey's institutional oversight capacity. Rare earth processing involving thorium and uranium presents hazards that are significantly more complex and persistent than those associated with conventional mining.

Turkey's mining sector is governed primarily by the Mining Law and its successive amendments, most significantly those of 2004 and 2010. REEs have been formally designated as strategic minerals under the Mining Law, placing their extraction and export under the direct oversight of the Ministry of Energy and Natural Resources.47 This classification is intended to ensure state control over resource development, promote domestic processing over raw ore export, and reduce dependence on foreign supply chains. By 2023, REE–related production, technology development, and trade activities were being monitored under the coordination of the Presidency’s Strategy and Budget Directorate and the Ministry of Energy and Natural Resources.48 Eti Maden, the public mining enterprise, has been designated as the operator of the Beylikova site.

The institutional architecture has been expanded to support REE development. TENMAK (Turkey’s Energy, Nuclear and Mining Research Authority) oversees NATEN, the Rare Earth Elements Research Institute, which was established in 2020 to anchor domestic research and development in rare earth processing.49 TÜBİTAK is involved in research on rare earth recovery and processing technologies, with broader efforts to develop domestic separation capabilities taking place alongside initiatives led by entities such as Eti Maden.50

Rare earth processing carries environmental risks qualitatively distinct from those associated with most other forms of mining, and the Beylikova ore presents risks with particular intensity. The deposit contains thorium and uranium — naturally occurring radioactive elements typically found in association with REE-bearing minerals — which require specialist regulatory treatment entirely different from that applicable to conventional mining waste. Turkey has no prior institutional experience with thorium management at commercial mining scale.

Turkey's current regulatory environment offers lower permitting barriers and less rigorous environmental compliance requirements than those prevailing in Western mining jurisdictions. This has been presented, implicitly, as a competitive advantage in attracting investment into the rare earth sector: Western rare earth producers have historically been disadvantaged relative to China precisely because their home jurisdictions impose environmental standards that raise costs. Over several decades, this contributed to China consolidating its dominance in REE processing.

This argument, however, is less persuasive in the current context. A permissive regulatory environment allows operators to defer safety investments and expand beyond licensed parameters, but when the resulting failure occurs, the financial consequences fall squarely on the company's balance sheet and share price. The Çöpler disaster involved a conventional cyanide heap-leach gold operation. A comparable incident at a rare earth processing site — one handling thorium-contaminated ore and industrial-scale volumes of acid leachate, the consequences of which would be both more persistent and more geographically diffuse — would generate environmental liabilities, regulatory consequences, and investor losses of a qualitatively greater magnitude.

First, environmental incidents can impose exceptionally high financial costs. The Çöpler case puts concrete numbers on this: $250–$300 million in remediation costs, a 53.7% single-day share price collapse, a 33% revenue decline, and an 80% production drop — all from a conventional gold operation.51 A rare earth incident involving radioactive tailings would generate cleanup liabilities that substantially exceed those figures, because radioactive contamination cannot be simply excavated and moved; it requires long-term containment, monitoring, and in some cases permanent land sterilization. Those costs sit on the company's balance sheet regardless of what the regulatory environment permitted at the time of construction.

Second, environmental permits are fundamental to the continued operation of mining projects. A company that has cut corners on tailings management or wastewater containment can have its permits revoked suspending production entirely while remediation proceeds. During that suspension, fixed costs continue, debt service continues, and revenue stops. The faster a company wants to get back into production, the more leverage the regulator has, which means the negotiated remediation terms tend to be more expensive than prevention would have been.

Third, environmental liability follows the parent company internationally. SSR Mining is listed on NASDAQ and the Toronto Stock Exchange.52 The legal and financial exposure from Çöpler extended beyond Turkey: securities class action litigation was filed in U.S. courts on behalf of investors, while the sharp decline in SSR Mining’s share price underscored the extent of its exposure to international capital markets.53 A rare earth company operating in Turkey under a Western government partnership — with government-backed offtake commitments or EU supply agreements — may also have exposure, because those government partners would face their own political accountability for having backed a project that produced a radioactive contamination event.

The financial profile of rare earth development is structurally challenging in ways that are independent of Turkey's specific circumstances. The development timeline from resource discovery to full-scale production in the rare earth sector typically extends over 15–20 years, reflecting the cumulative duration of geological validation, feasibility studies, pilot processing, environmental permitting, infrastructure construction, and ramp-up to commercial capacity.54

Beylikova's reserves are not yet proven in the international sense. Adding the typical development timeline to the time still required to complete JORC certification implies that commercial-scale production from Beylikova appears unlikely before the mid-2030s under even favorable conditions. Even after operations commence, additional years are typically required for a project to reach financial break-even, making rare earth mining fundamentally incompatible with short-term investment horizons. Eti Maden’s plans to scale the Beylikova project to industrial rare earth processing capacity imply substantial upfront capital investment, with projected revenues of approximately $220 million annually only achievable once full production is reached.55

The financial returns on rare earth projects, once operational, are also constrained by market structure. Based on global production volumes and prevailing oxide prices reported by the U.S. Geological Survey, the rare earth market amounts to only a few billion dollars annually, underscoring its relatively small economic scale despite its strategic importance.56

China’s dominance in rare earth processing — accounting for roughly 90% of global refined supply — has enabled it to exert significant downward pressure on global prices through increases in domestic production quotas. Whether such moves reflect deliberate strategic intent to render competing investments uneconomical, or primarily serve domestic industrial objectives, is debated among analysts; the practical effect on non-Chinese producers has in either case been severe. A 25% increase in Chinese output in 2022 contributed to a sharp price decline that undermined competing projects. Molycorp, the United States’ largest rare earth company, had previously filed for bankruptcy in 2015 following an earlier period of Chinese price pressure, and several other Western projects have subsequently been suspended or abandoned when Chinese oversupply rendered them uneconomical.57 These "boom-and-bust" pricing cycles—whether reflecting deliberate strategy or domestic industrial policy decisions—represent a systemic risk that any Turkish operator would face from the moment production begins — and that would be most dangerous during the early years of operation, when debt servicing costs are highest, and the project has yet to reach sustained profitability.

Given these market realities, rare earth mining is rarely viable as a purely private-sector initiative. State intervention — through price guarantees or floor pricing, long-term offtake agreements, subsidized financing, and strategic stockpiling programs — plays a central role in sustaining the industry wherever it has taken root outside China. Without such measures, private investors are unlikely to commit capital to projects with uncertain and distant returns.

For Turkey, state-backed price support and offtake arrangements would likely be essential conditions for attracting and retaining credible operators, particularly during periods of global price suppression. Eti Maden is wholly state-owned and currently designated as the project operator, which provides a degree of insulation from purely private commercial influence. Any Turkish production facility would need to be able to sustain operations through such periods, either through a government-backed price floor or long-term offtake agreements. One example is the United States’ arrangement with MP Materials, which guarantees a minimum price of $110 per kilogram of neodymium-praseodymium oxide.58

This implies a substantial and long-term fiscal commitment on the part of the Turkish government. Rare earth projects should therefore be evaluated not primarily on financial returns — which are modest relative to the capital involved — but on their strategic value for industrial policy, supply chain security, and technological sovereignty.

The more commercially significant risk sits at the level of subcontracting, technology transfer agreements, and construction partnerships: the decisions about who builds the industrial facility, who provides the processing technology, and who secures the downstream manufacturing agreements represent a concentration of economic value that may increase exposure to political influence and patronage networks. In Turkish politics, large state-controlled resource projects have at times functioned not only as instruments of industrial policy but also as mechanisms shaped by political patronage networks.

The Çöpler mine disaster illustrates the potential consequences such governance dynamics can create for Western partners. The Çöpler mine was operated by Anagold Madencilik,59 a joint venture between SSR Mining and Lidya Madencilik, a subsidiary of Çalık Holding,60 a conglomerate widely regarded as having close ties to the Erdoğan government.61 Subsequent investigations and expert assessments indicated that the heap-leach pad had exceeded its approved EIA capacity and that warning signals had not been adequately addressed.62 The Turkish government-led parliamentary inquiry concluded with no assignment of political responsibility, classifying the collapse as a geotechnical failure, while the ministers implicated remained in office and Çalık Holding continued to receive major government infrastructure contracts after the disaster.

The critical observation is that political protection in Turkey is asymmetric. It protected the locally connected partner from Turkish institutional consequences. It did not, however, protect SSR Mining. SSR Mining absorbed the financial consequences: a 53.7% single-session share price collapse, erasing over $1 billion in shareholder value, and a US securities class action lawsuit.

Screenshot of the official Anagold Madencilik website detailing historical and current parameters of the Çöpler Gold Mine infrastructure. Source: Anagold Madencilik

The technology transfer dimension introduces a second and distinct commercial risk. A Western company committing proprietary processing technology to a partnership in Turkey will require that its counterpart have the technical capacity to absorb and develop that knowledge productively. Transparency International's assessment of Turkey's national integrity system identifies state-owned enterprises as among the weakest institutional categories in Turkey's governance architecture, scoring just 24 out of 100, reflecting political interference, lack of meritocratic staffing, and insufficient operational independence.63 If staffing and procurement decisions at Beylikova are driven by political connections rather than technical competence, technology would be transferred into an environment where it cannot be effectively deployed.

Contract enforceability compounds both risks. A company signing offtake agreements, price floors, or supply commitments with a Turkish state entity over a multi-decade horizon needs those contracts to be enforceable by an independent judiciary if circumstances change. Turkey ranked 118th out of 143 countries in the World Justice Project's 2025 Rule of Law Index.64 Transparency International notes that the executive still appoints the majority of members of the Council of Judges and Prosecutors without transparent competitive procedures, and that no reform has been initiated despite recurring recommendations.65 The US State Department's Investment Climate Statement for Turkey notes that anti-bribery enforcement is uneven and that large public contracts continue to be awarded to firms with AKP connections.66

If the contractual framework remains enforceable only as long as the underlying political relationship holds, foreign investors face significant long-term uncertainty. Over the lifespan of a rare earth processing facility, this would mean committing billions of dollars on the basis of legal protections contingent on political alignment rather than independent judicial enforcement. The Çöpler case is instructive here, too. The US securities class action against SSR Mining (Akhras v. SSR Mining Inc., No. 1:24-cv-00739, D. Colo.) was filed on the basis that the company had made materially false and misleading statements to investors about its safety practices.67 The complaint alleged that the defendants materially overstated SSR Mining's commitment to safety and the efficacy of its safety measures, and that the company engaged in unsafe mining practices that were reasonably likely to result in a mining disaster.

The legal exposure did not require the company itself to have bribed anyone; rather, it arose from the consequences of operating in a governance environment where its partner's political protection substituted for regulatory compliance, and where the company failed to disclose that substitution adequately to its shareholders. The case has since progressed through a motion to dismiss. In September 2025, the court granted the defendants' motion to dismiss without prejudice, but also granted the plaintiff leave to file an amended complaint.68

Rent extraction introduces a further cost-structure problem. The Turkish government has long been accused of channeling public resources toward politically connected companies while sidelining rivals.69 Confiscated assets under the management of the Savings Deposit Insurance Fund of Turkey (TMSF) included more than 1,000 businesses in 2025, though this figure fluctuates annually as companies are seized by the government and sold off for a variety of reasons, giving it significant influence over Turkey's corporate landscape.70

Finally, Western companies operating under the US Foreign Corrupt Practices Act, the UK Bribery Act, or equivalent frameworks face direct legal exposure if their Turkish joint venture partners engage in the kind of politically facilitated procurement practices described above. Due diligence obligations extend to the conduct of partners and intermediaries, not only to the company's own conduct. A Western company that cannot satisfy its own legal counsel that the partnership is free of conduct that could trigger liability under the FCPA will not enter the partnership, regardless of how attractive the ore deposit is. Turkey’s state subsidy system has been documented as disproportionately benefiting a small number of politically connected companies.71

A foreign company that cannot see a clear institutional separation between Beylikova's development decisions and the patronage dynamics of Turkey's current political economy may not commit the capital and technology the project requires, regardless of the scale of the deposit. Accountability and the rule of law are essential considerations in assessing these commercial risks.

Turkey's Beylikova deposit contains elements that are in high demand across the green energy, electric vehicle, and defense sectors. Western governments have committed substantial public financing to secure non-Chinese rare earth supply chains, and Turkey has taken initial steps to position itself within that landscape. A credible technology partnership that would allow Turkey to process rather than simply export its ore remains the central condition for realizing that potential. This section examines the market conditions, financing landscape, and technology transfer options that define the opportunity available to Turkey.

The elements present in Turkey's Beylikova deposit serve industrial applications whose demand trajectories are structurally supported by the green energy transition, the electrification of transport, and the expansion of advanced defense systems.

For Turkey's specific ore profile, a significant application is permanent magnet production for electric vehicles and wind turbines. As Professor Mustafa Kumral, Dean of the Faculty of Mining at Istanbul Technical University, has noted, the "magnet suite" of elements (neodymium, praseodymium, dysprosium, and terbium) represents more than 90% of the global REE trade value despite constituting a small portion of total volume, adding that “Turkey must build a full ecosystem that connects resources to research, production, and diplomacy.”72

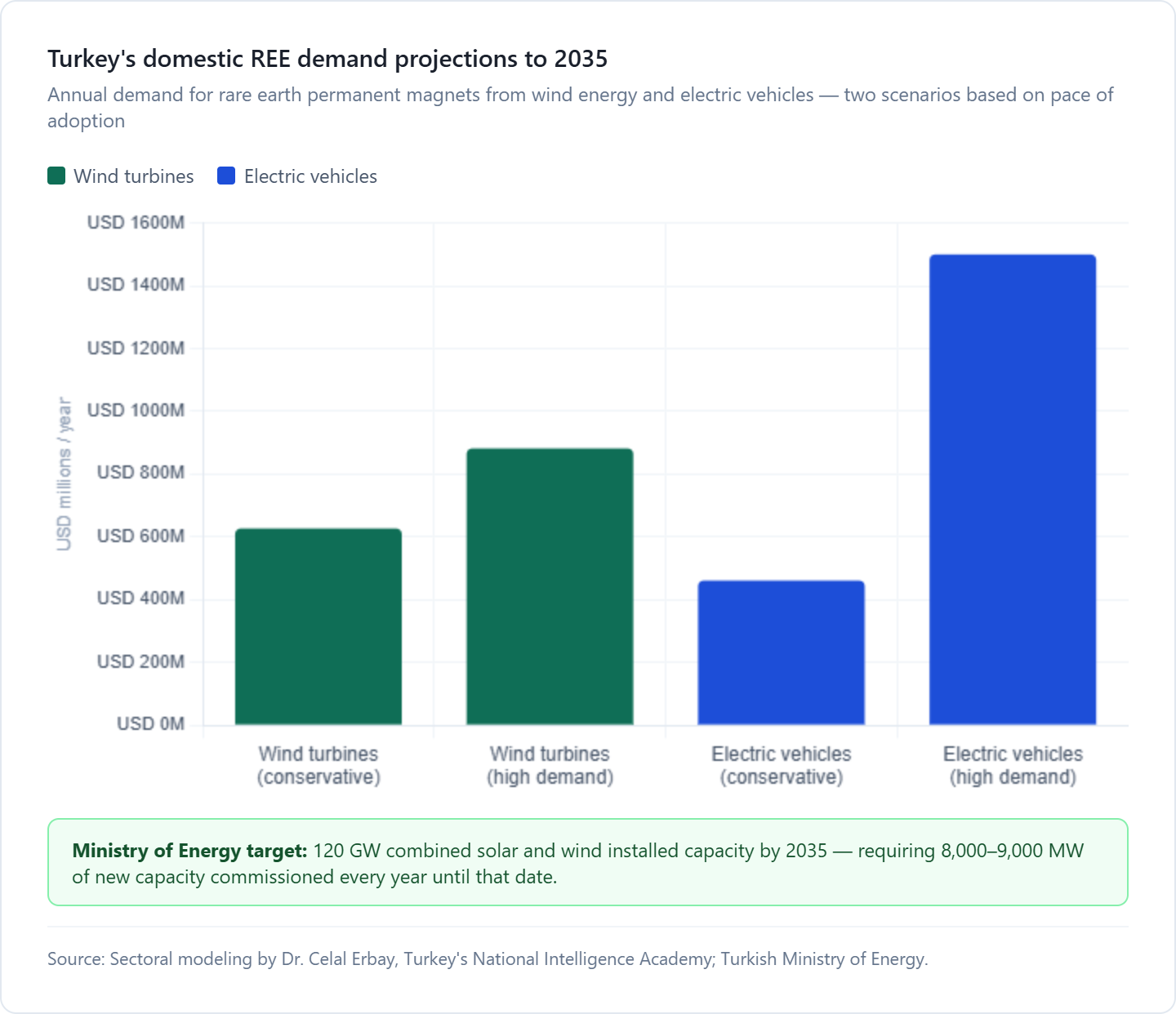

In this regard, Turkey's own renewable energy targets create a significant domestic demand base. The Ministry of Energy has set a combined solar and wind installed capacity goal of 120 gigawatts by 2035, a target that requires the commissioning of between 8,000 and 9,000 megawatts of new capacity every year until that date.73 According to sectoral modeling by Dr. Celal Erbay of Turkey's National Intelligence Academy, the country's combined wind and electric vehicle sectors could require permanent magnets costing in excess of $2 billion annually by 2035 under a high-demand scenario, with wind turbines alone accounting for between $627 million and $882 million and the electric vehicle sector adding between $461 million and $1.5 billion depending on the pace of adoption.74

The defense applications of Turkey's ore add a further dimension. REEs are embedded throughout modern weapons systems: a single F-35 fighter jet contains over 920 pounds of rare earth materials; an Arleigh Burke-class destroyer requires more than 5,700 pounds; a Virginia-class submarine depends on more than 10,000 pounds.75 Turkey's expanding domestic defense industrial base — producing unmanned aerial vehicles, guided munitions, and radar systems each containing REE components — creates a strategic rationale for domestic supply chain development that extends well beyond purely commercial considerations. If Turkey were to supply both its own industry with domestically processed rare earth materials, the geopolitical value of that contribution would exceed its market valuation.

The geopolitical context Turkey is stepping into has created a strong and unusually broad appetite for public financing of rare earth projects outside China. Beijing’s April 2025 export controls on seven heavy REEs—samarium, gadolinium, terbium, dysprosium, lutetium, scandium, and yttrium, introduced in response to U.S. tariffs—made the risks of supply concentration especially clear.76 The November 2025 expansion of controls to include processing equipment further heightened the urgency, extending supply risks beyond raw materials to the technologies required to refine them.

Against this backdrop, both the United States and the European Union have committed to supporting non-Chinese rare earth supply chains with levels of public financing that would have been difficult to imagine a decade ago. In the United States, the Department of Defense has awarded over $439 million to rare earth processing and magnet manufacturing companies since 2020 under the Defense Production Act, with funds directed to Lynas USA for heavy and light rare earth separation facilities in Texas, MP Materials for rare earth metal, alloy, and magnet manufacturing in Fort Worth, and Noveon Magnetics for magnet production in San Marcos.77 In July 2025, the Pentagon concluded a multibillion-dollar public-private partnership with MP Materials that made the US government the company's largest shareholder through a $400 million preferred stock acquisition, extended a $150 million loan for heavy rare earth separation expansion, committed to purchasing 100% of the output of its new magnet factory, and establishes a price floor of $110 per kilogram for neodymium-praseodymium to shield the company from Chinese price suppression.78

The US Export-Import Bank, meanwhile, has offered $160 million in debt financing for Pensana's Angolan rare earth mine79 — a figure that substantially exceeds the approximately $6.6 million the UK government offered for the same project's processing facility, prompting the company to abandon its British plans and reorient entirely toward the United States.80

In Europe, the EU's Critical Raw Materials Act, which entered into force in May 2024, sets benchmark targets for domestic extraction, processing, and recycling of strategic minerals by 2030, specifically at least 10% of annual consumption from domestic extraction, 40% from domestic processing, and 25% from recycling, while capping dependence on any single third country at 65%.81 The Global Gateway infrastructure program has created additional financing channels for supply chain partnerships with allied countries.82

Australia's parliament passed a 10% production tax credit for critical minerals processing in February 2025, with the incentive applicable from 2027.83 Japan's JOGMEC acquired a 65% stake in Lynas Rare Earths' production volume for approximately $131 million, securing priority supply rights through 2038.84

Turkey has taken initial steps to position itself within this funding landscape. Following the collapse of negotiations with China and Russia, Ankara has turned to the United States as its primary prospective partner, with Bloomberg reporting in October 2025 that Turkish officials are pursuing a partnership with Washington for the Beylikova deposit.85

Turkey is a member of the Minerals Security Partnership (MSP) Forum, a US-led plurilateral initiative aimed at accelerating the development of diverse and sustainable critical minerals supply chains, and has been in active discussions with the United States on critical minerals cooperation following the September 2025 Trump-Erdoğan meeting, with potential channels to Export-Import Bank financing and Defense Production Act investment under discussion.86 Turkey is also in talks with Canada and Switzerland on potential cooperation, including feasibility studies needed to advance the project.87

Even assuming full reserve verification, Turkey would face severe technological challenges. The commercial value of REEs does not lie in their extraction from the ground, which is technically the least demanding step in the supply chain. It lies in the subsequent stages of chemical separation, oxide production, metal refining, alloy manufacturing, and — at the apex of the value chain — permanent magnet production. This sequence involves approximately one hundred distinct processing steps, requiring specialized knowledge in hydrometallurgy, solvent extraction chemistry, and metallurgical engineering. Processing costs range from $20 to $100 per kilogram of rare earth oxide, depending on ore composition, with approximately two-thirds of the total cost arising from the separation and purification stages alone.88 Chinese producers operate at costs of $11 or less per kilogram of rare earth oxide, a benchmark that non-Chinese operators — facing higher labor costs, stricter environmental compliance requirements, and the absence of decades of accumulated economies of scale — cannot currently approach.89

Turkey currently possesses none of this capability at a commercial scale. Associate Professor Salih Cihangir of Munzur University, who has assessed the Beylikova project, confirms that Turkey has progressed to laboratory and, to a lesser extent, pilot-scale production of some purified fractions, but emphasizes that scaling to high-value commercial production requires achieving milestones in bulk separation, individual REE oxide isolation, and rigorous environmental, health, and safety protocols.90 The knowledge required to close this gap would have to come through technology transfer from a partner with deep processing expertise.

The difficulty is that such partners are either unwilling to transfer their knowledge on terms consistent with Turkey's strategic interests or constrained from doing so. China is the world's dominant technology holder in rare earth processing, controlling approximately 85% of global refining capacity and more than 90% of permanent magnet production.91 On December 21, 2023, Beijing imposed a comprehensive ban on the export of rare earth extraction and separation technologies.92 In October 2025, China further tightened restrictions by requiring foreign firms to obtain government approval to export magnets containing even trace amounts of Chinese-origin rare earth materials. Beijing also barred Chinese nationals from supporting overseas rare earth projects without authorization and denied export licenses to firms affiliated with foreign militaries.93 These moves were explicitly designed to prevent the development of competitive midstream capacity anywhere outside China's influence.

Turkey's October 2024 memorandum of understanding with Beijing on natural resources and mining cooperation, signed by Energy Minister Bayraktar and China's Minister of Natural Resources Wang Guanghua, appeared to offer a shortcut to the processing expertise Turkey lacks, as China holds the deepest technical knowledge in the sector.94 However, what the negotiations revealed was that China's interest in Beylikova was not in helping Turkey develop a domestic processing industry but in securing access to the ore itself. Chinese negotiators insisted on terms that would require transporting the extracted material to China for refining rather than permitting local processing, and refused to transfer the processing technology.95

Furthermore, China's October 2025 announcement of export controls covering processing and separation equipment,96 suspended for one year in November 2025 as part of a diplomatic agreement, but with the underlying regulatory framework left intact.97 This has demonstrated that Turkey cannot assume reliable access to Chinese capital equipment for its processing facility. The policy reflected what analysts describe as a deliberate shift from volume control to capability control, designed to preserve China's technological leadership even as new mining projects emerge elsewhere.98

Turkey’s long-term interest lies in developing indigenous processing capability, not in becoming a raw ore exporter. Whether Western partners will agree, however, depends on their own assessment of Turkey’s reserve quality, governance standards, and strategic reliability. Turkey has since turned its attention to Western partners. Feasibility studies are underway with entities in Canada and Switzerland. Energy Minister Bayraktar has stated that Turkey is in active negotiations with the United States, Canada, Australia, and Europe, with the condition that any technology partner must agree to knowledge transfer and local production requirements.99

In a letter to the Grand National Assembly dated 8 January 2026, Minister of Energy and Natural Resources Alparslan Bayraktar confirmed that China, the United States, Australia, and Canada treat rare earth processing technology as a strategic and competitive asset and decline to share it.100 According to the letter, no technology transfer agreement has been concluded with any foreign party. Contacts with the United States remain, the Minister noted, at the level of general consultations. To address this constraint, Bayraktar stated that the government is pursuing domestic capability through TENMAK, which has established rare earth ore enrichment, purification, and permanent magnet production laboratories, as well as through research collaboration agreements with Turkish universities.

Minister Bayraktar's Letter to Parliament on Turkey's Rare Earth Strategy

Turkish Minister of Energy and Natural Resources Alparslan Bayraktar outlining Turkey's rare earth elements strategy in a written response to the Grand National Assembly, 3 January 2026. The Minister confirmed the Beylikova pilot facility was operational and that industrial-scale engineering was planned from 2027, but conceded that the countries dominating rare earth processing — China, the United States, Australia, and Canada — treat their technological expertise as a strategic and competitive asset, refusing to share it. Turkey's response, the Minister indicated, is to build domestic capacity through TENMAK and university partnerships, while pursuing international cooperation on its own terms.

In this regard, the Japan-Lynas partnership offers a potential model for the kind of arrangement Turkey could pursue. In 2023, the Japan Organization for Metals and Energy Security (JOGMEC) acquired a 65% stake in Lynas Rare Earths' production volume, investing approximately $131 million in exchange for priority supply rights to Lynas's growth capacity until 2038.101 Nonetheless, building a technology partnership of genuine depth with a Western counterpart would take years even under favorable conditions.

A risk for Turkey is that Western commitments remain aspirational while Chinese capital moves at an industrial scale. Western firms have demonstrated significantly less processing expertise than China and, in several cases, are only now beginning to build their own midstream capabilities. As Arman Sidhu has argued in an opinion piece published by Institute for Diplomacy and Economy (instituDE), when Australia's Syrah Resources idled its Balama graphite mine in Mozambique amid weak prices and Chinese oversupply, China's DH Mining filled the resulting vacuum with a $200 million, 25-year investment — inaugurating a 200,000-metric-ton-per-year processing plant at full industrial scale.102

It is also an open question whether Western governments would be willing to depend on Turkey as a critical supply chain node, given Turkey’s documented track record of leveraging strategic assets as instruments of geopolitical pressure and its unsteady relationship with both Washington and Brussels under President Erdoğan.

Turkey enters the rare earth sector at a moment of historically favorable external conditions: acute Western demand for non-Chinese supply chain alternatives, unprecedented willingness to deploy public capital in their support, and a geopolitical environment in which Turkey's geographic and political position gives it genuine leverage in negotiations with both Western and Chinese partners. The Beylikova deposit, if its scale and grade are confirmed through rigorous international certification, would represent a meaningful addition to global non-Chinese rare earth reserves and may constitute one of the more significant non-Chinese REE partnerships available to supply chains.

The obstacles, however, are formidable and should not be minimized. The reserve remains unverified by international standards, a condition that is foundational to attracting serious investment. The processing technology required for commercial-scale refining is not domestically available, talks with China have collapsed over technology transfer terms, and Western alternatives are still developing their own capabilities. The radioactive complexity of the Beylikova ore demands environmental governance capabilities that Turkey's institutions have not previously been required to exercise, and the domestic mining sector's track record, illustrated most starkly by the preventable İliç disaster of 2024, does not provide automatic reassurance that those capabilities will be built. The economics of rare earth development, with investment timelines of fifteen or more years from proven reserve to commercial operation and a commodity market subject to price manipulation, are unforgiving of weakness.

The governance and political economy conditions under which Beylikova would be developed add a further layer of difficulty. Western partners operating under anti-corruption frameworks cannot enter arrangements in which political connections substitute for regulatory compliance. The reforms required to attract credible investment are the same reforms that the rule of law and democratic accountability require on their own terms.

The realistic assessment is that Turkey will not be a significant actor in global rare earth markets within a decade under any scenario. The lead times are too long, and the institutional development required is too substantial for that horizon to be achievable, regardless of the policy decisions made today. What those decisions will determine is whether Turkey is positioned to become a meaningful actor in the decade that follows.

[1] William F. Burkhart and Keigh E. Hammond, "Presidential 2025Tariff Actions: Timeline and Status," CRS Report R48549 (Washington, DC:Congressional Research Service, January 12, 2026), https://www.congress.gov/crs-product/R48549.

[2] Victor Loh,"China 'Not Afraid of Trade War,' Accuses U.S. of 'Double Standard' forRare Earths Retaliation," CNBC, October 12, 2025, https://www.cnbc.com/2025/10/12/china-defends-rare-earth-export-curbs-as-legitimate-hits-back-at-us-tariffs-ahead-of-possible-trump-xi-meeting.html.

[3] Tae-Yoon Kim, Shobhan Dhir, Amrita Dasgupta,and Alessio Scanziani, "With New Export Controls on Critical Minerals,Supply Concentration Risks Become Reality," International Energy Agency,October 23, 2025, https://www.iea.org/commentaries/with-new-export-controls-on-critical-minerals-supply-concentration-risks-become-reality.

[4] Megan Cerullo,"Ford CEO Says Rare Earths Shortage Forced It to Shut Factory," CBSNews, June 13, 2025, https://www.cbsnews.com/news/ford-ceo-china-rare-earth-shortage-car-production/.

[5] Christina Lu,"Trump's Chaotic Agenda Has a Critical Through Line," ForeignPolicy, February 26, 2025, https://foreignpolicy.com/2025/02/26/trump-rare-earth-critical-mineral-resource-ukraine-greenland-canada/.

[6] "Turkey ToutsDiscovery of World's 2nd-Largest Rare Element Reserve," Daily Sabah,July 12, 2022, https://www.dailysabah.com/business/energy/turkey-touts-discovery-of-worlds-2nd-largest-rare-element-reserve.

[7] "Türkiye EyesTop 5 Rank Among Rare Earth Producers via Partnerships," Daily Sabah,October 19, 2025, https://www.dailysabah.com/business/energy/turkiye-eyes-top-5-rank-among-rare-earth-producers-via-partnerships.

[8] Nadir Toprak Elementleri ve Türkiye: Jeopolitik Satrançta Yeni Dinamiklerve Aktörler (Ankara:Millî İstihbarat Akademisi, Mayıs 2025), 20, https://mia.edu.tr/uploads/f/30052025_1.pdf.

[9] Mustafa Enes Esen,"Geopolitical Constraints of Turkey's Energy Hub Ambitions,"Institute for Diplomacy and Economy (instituDE), July 8, 2025, https://www.institude.org/report/geopolitical-constraints-of-turkeys-energy-hub-ambitions.

[10] Deniz Açık, "Beylikova Florit, Barit ve Nadir Toprak ElementleriTesisi Açılıyor," Anadolu Ajansı, April 18, 2023, https://www.aa.com.tr/tr/bilim-teknoloji/beylikova-florit-barit-ve-nadir-toprak-elementleri-tesisi-aciliyor/2875143.

[11] "Cumhurbaşkanı Erdoğan, Kabine Toplantısı'nın Ardından MilleteSeslendi," Türkiye Cumhurbaşkanlığı İletişim Başkanlığı, October15, 2025, https://www.iletisim.gov.tr/turkce/haberler/detay/cumhurbaskanligi-kabinesi-cumhurbaskani-erdogan-baskanliginda-toplandi-15-10-25.

[12] MTA E-Ticaret Sitemiz: Hakkımızda, Maden Tetkik ve Arama Genel Müdürlüğü (MTA), accessed via https://eticaret.mta.gov.tr/index.php?route=information/information&information_id=4.

[13] Maden Kanununda ve Bazı Kanunlarda Değişiklik Yapılmasına İlişkin Kanun, Kanun No. 5177, kabul tarihi 26 Mayıs2004, Resmî Gazete, 5 Haziran 2004, Sayı 25483, https://www5.tbmm.gov.tr/tutanaklar/KANUNLAR_KARARLAR/kanuntbmmc088/kanuntbmmc088/kanuntbmmc08805177.pdf.

[14] Tuğçe Yılmaz and Vecih Cuzdan, "Beylikova'daki Nadir ToprakElementleri Rezervine Dair: Bilinenler ve Bilinemeyenler," Bianet,October 9, 2025, https://bianet.org/haber/beylikovadaki-nadir-toprak-elementleri-rezervine-dair-bilinenler-ve-bilinemeyenler-312389.

[15] Türkiye Kritik veStratejik Madenler Raporu (Ankara: T.C. Enerji ve Tabii Kaynaklar Bakanlığı,2025), https://enerji.gov.tr/Media/Dizin/TKDB/tr/Belgeler/Tu%CC%88rkiye_Kritik_ve_Stratejik_Madenler_Raporu.pdf.

[16] Tuğçe Yılmaz and Vecih Cuzdan, "Beylikova'daki Nadir ToprakElementleri Rezervine Dair: Bilinenler ve Bilinemeyenler," Bianet,October 9, 2025, https://bianet.org/haber/beylikovadaki-nadir-toprak-elementleri-rezervine-dair-bilinenler-ve-bilinemeyenler-312389.

[17]Australasian JointOre Reserves Committee (JORC), "What Is the JORC Code?," JORC, https://www.jorc.org/.

[18] Sinan Tavsan,"Turkey Unveils Rare Earth Find, Seeks Partners Amid China-USRivalry," Nikkei Asia, October 28, 2025, https://asia.nikkei.com/business/materials/turkey-unveils-rare-earth-find-seeks-partners-amid-china-us-rivalry.

[19] U.S. GeologicalSurvey, Mineral Commodity Summaries 2025, ver. 1.2 (Reston, VA: U.S.Geological Survey, March 2025), 212 p., https://doi.org/10.3133/mcs2025.

[20] A Rare Earth Mirage — ora Strategic Pivot? Türkiye's 2026 Energy Push Under the InvestorMicroscope," Rare Earth Exchanges, December 31, 2025, https://rareearthexchanges.com/news/a-rare-earth-mirage-or-a-strategic-pivot-turkiyes-2026-energy-push-under-the-investor-microscope/.

[21] "Türkiye'nin 694 Milyon Tonluk Nadir Toprak Elementleri Rezervi İçinYabancı Uzmanlar Ne Diyor?" Euronews Türkçe, July 16, 2022, https://tr.euronews.com/2022/07/16/turkiyenin-694-milyon-tonluk-nadir-toprak-elementleri-rezervi-icin-yabanci-uzmanlar-ne-diy.

[22] "Türkiye'nin 694 Milyon Tonluk Nadir Toprak Elementleri Rezervi İçinYabancı Uzmanlar Ne Diyor?" Euronews Türkçe, July 16, 2022.

[23] "Türkiye EyesTop 5 Rank Among Rare Earth Producers via Partnerships," Daily Sabah,October 19, 2025, https://www.dailysabah.com/business/energy/turkiye-eyes-top-5-rank-among-rare-earth-producers-via-partnerships.

[24] Nadir Elementler veTürkiye'nin Beylikova Keşfi (Istanbul: Kuveyt Türk Yatırım, October 21, 2025), https://kuveytturkyatirim.com.tr/media/ipej0smq/nadir-elementler-ve-tuerkiyenin-beylikova-ke%C5%9Ffi.pdf.

[25] A Rare Earth Mirage— or a Strategic Pivot? Türkiye's 2026 Energy Push Under the InvestorMicroscope," Rare Earth Exchanges, December 31, 2025, https://rareearthexchanges.com/news/a-rare-earth-mirage-or-a-strategic-pivot-turkiyes-2026-energy-push-under-the-investor-microscope/.

[26] "Boron,"Republic of Türkiye Ministry of Energy and Natural Resources, https://enerji.gov.tr/infobank-naturalresources-boron.

[27] "Hakkımızda," Türkiye Enerji, Nükleer ve Maden Araştırma Kurumu(TENMAK), https://www.tenmak.gov.tr/hakkimizda.

[28] "€3.5T Worth ofUnearthed Mine Reserves Lie Beneath Türkiye, Sector Head Says," TürkiyeToday, August 19, 2025, https://www.turkiyetoday.com/business/35t-worth-of-unearthed-mine-reserves-lie-beneath-turkiye-sector-head-says-3205630.

[29] Petra Zapp, AndreaSchreiber, Josefine Marx, et al., "Environmental Impacts of Rare EarthProduction," MRS Bulletin 47 (March 2022): 267–275, https://doi.org/10.1557/s43577-022-00286-6.

[30] Zapp, Schreiber,Marx, et al., "Environmental Impacts of Rare Earth Production."

[31] Jaya Nayar,"Not So 'Green' Technology: The Complicated Legacy of Rare EarthMining," Harvard International Review, August 12, 2021, https://hir.harvard.edu/not-so-green-technology-the-complicated-legacy-of-rare-earth-mining/.

[32] Tailings ProgressReport: Implementing the Global Industry Standard on Tailings Management(GISTM) (London: International Council on Mining andMetals, November 5, 2025), https://www.icmm.com/en-gb/research/tailings-management/2025/tailings-progress-report.

[33] Tuğçe Yılmaz and Vecih Cuzdan, "Beylikova'daki NTE Rezervlerinin NedenOlabileceği Tehlike: Toryum ve Diğer Kimyasal Atıklar," Bianet,October 10, 2025, https://bianet.org/haber/beylikovadaki-nte-rezervlerinin-neden-olabilecegi-tehlike-toryum-ve-diger-kimyasal-atiklar-312422.

[34] Gracelin Baskaranand Meredith Schwartz, "Developing Rare Earth Processing Hubs: AnAnalytical Approach," Center for Strategic and International Studies, July28, 2025, https://www.csis.org/analysis/developing-rare-earth-processing-hubs-analytical-approach.

[35] Nayar, "Not So'Green' Technology."

[36] Laura Bicker and theVisual Journalism Team, "Poisoned Water and Scarred Hills: The Price ofthe Rare Earth Metals the World Buys from China," BBC News, August7, 2025, https://www.bbc.co.uk/news/resources/idt-66cdf862-5e96-4e6e-90b8-a407b597c8d9.

[37] Emily Fishbein andJauman Naw, "In Myanmar, Illicit Rare Earth Mining Is Taking a HeavyToll," Yale Environment 360, November 20, 2025, https://e360.yale.edu/features/myanmar-rare-earth-mining.

[38] Yong-He Han, Xi-WenCui, Yong Zhang, Hong Zhang, Zhibiao Chen, et al., "Environmental Impactsof Rare Earth Elements Mining and Strategies for Sustainable Management: AComprehensive Review," Journal of Hazardous Materials 500 (December5, 2025): 140400, https://www.sciencedirect.com/science/article/abs/pii/S0304389425033205.

[39] J. Bai, X. Xu, Y.Duan, et al., "Evaluation of Resource and Environmental Carrying Capacityin Rare Earth Mining Areas in China," Scientific Reports 12 (April12, 2022): 6105, https://doi.org/10.1038/s41598-022-10105-2.

[40] "Turkey RescuersBattle to Save Workers Trapped in Landslide-Hit Gold Mine," Al Jazeera,February 14, 2024, https://www.aljazeera.com/news/2024/2/14/turkey-rescuers-battle-to-save-workers-trapped-in-landslide-hit-gold-mine.

[41] Madhurima Das,"SSR Mining Declines 39% YTD: How Should You Play the Stock Now?" YahooFinance, October 23, 2024, https://finance.yahoo.com/news/ssr-mining-declines-39-ytd-165500295.html.

[42] SSR Mining Inc.,"SSR Mining Reports Fourth Quarter and Full-Year 2024 Results," newsrelease, February 18, 2025, https://www.ssrmining.com/_resources/pdfs/SSR-Mining-Reports-Fourth-Quarter-and-Full-Year-2024-Results.pdf.

[43] SSR Mining Inc.,"SSR Mining Reports Second Quarter 2024 Results," news release, July31, 2024, https://www.juniorminingnetwork.com/junior-miner-news/press-releases/802-tsx/ssrm/164996-ssr-mining-reports-second-quarter-2024-results.html.

[44] Thames Menteth,"Turkey Gold Mine Landslide Site Was Moving 4 Years Before Failure, StudyFinds," Ground Engineering, May 20, 2025, https://www.geplus.co.uk/news/turkey-gold-mine-landslide-site-was-moving-4-years-before-failure-study-finds-20-05-2025/.

[45] Mariaan Webb,"Çöpler Temporarily Suspended, SSR Confirms," Mining Weekly,June 29, 2022, https://www.miningweekly.com/article/pler-temporarily-suspended-ssr-confirms-2022-06-29.

[46] Abdullah Bozkurt,"Environmental Rubber-Stamping in Erdoğan's Turkey: A System Built toFail," Nordic Monitor, May 12, 2025, https://nordicmonitor.com/2025/05/environmental-rubber-stamping-in-erdogans-turkey-a-system-built-to-fail/.

[47] T.C. Enerji ve Tabii Kaynaklar Bakanlığı, Türkiye Kritik ve StratejikMadenler Raporu (Ankara: T.C. Enerji ve Tabii Kaynaklar Bakanlığı, 2025), https://enerji.gov.tr/Media/Dizin/TKDB/tr/Belgeler/Tu%CC%88rkiye_Kritik_ve_Stratejik_Madenler_Raporu.pdf.

[48] "Türkiye'nin Nadir Toprak Elementleri Politikası," KültürMedeniyet Vakfı, https://kumevakfi.org/turkiye-nadir-toprak-elementleri-politikasi.

[49] "Hakkımızda,"Türkiye Enerji, Nükleer ve Maden Araştırma Kurumu (TENMAK), https://www.tenmak.gov.tr/hakkimizda.

[50] Mahmut Özer, "TÜBİTAK'ın Nadir Toprak Elementleri ve Çip ÜretimineYaklaşımı," Milliyet, February 16, 2026, https://www.milliyet.com.tr/yazarlar/prof-dr-mahmut-ozer/tubitakin-nadir-toprak-elementleri-ve-cip-uretimine-yaklasimi-7538830.

[51] SSR Mining Inc.,"SSR Mining Reports Fourth Quarter and Full-Year 2024 Results," newsrelease, February 18, 2025, https://www.ssrmining.com/_resources/pdfs/SSR-Mining-Reports-Fourth-Quarter-and-Full-Year-2024-Results.pdf.

[52] "About SSRMining," SSR Mining Inc., https://www.ssrmining.com/company/.

[53] Hagens Berman SobolShapiro LLP, "SSR Mining (SSRM) Stock Drop After Landslide at Çöpler MineTriggers Investor Lawsuit – Hagens Berman," GlobeNewswire, May 6, 2024, https://www.globenewswire.com/news-release/2024/05/06/2876094/32716/en/SSR-Mining-SSRM-Stock-Drop-After-Landslide-at-%C3%87%C3%B6pler-Mine-Triggers-Investor-Lawsuit-Hagens-Berman.html.

[54] Paul Manalo,"Average Lead Time Almost 18 Years for Mines Started in 2020–23,"S&P Global Market Intelligence, April 10, 2024, https://www.spglobal.com/market-intelligence/en/news-insights/research/average-lead-time-almost-18-years-for-mines-started-in-2020-23.

[55] "Türkiye EyesTop 5 Rank Among Rare Earth Producers via Partnerships," Daily Sabah,October 19, 2025, https://www.dailysabah.com/business/energy/turkiye-eyes-top-5-rank-among-rare-earth-producers-via-partnerships.

[56] Shelby N. Johnston,"Rare Earths," in Mineral Commodity Summaries 2026 (Reston,VA: U.S. Geological Survey, February 2026), https://pubs.usgs.gov/periodicals/mcs2026/mcs2026-rare-earths.pdf.

[57] Jon Emont, "HowChina Took Over the World's Rare-Earths Industry," The Wall StreetJournal, October 19, 2025, https://www.wsj.com/economy/trade/how-china-took-over-the-worlds-rare-earths-industry-fb668839.

[58] Tom Moerenhout,"MP Materials Deal Marks a Significant Shift in US Rare EarthsPolicy," Center on Global Energy Policy, Columbia University, July 11,2025, https://www.energypolicy.columbia.edu/mp-materials-deal-marks-a-significant-shift-in-us-rare-earths-policy/.

[59] "OxideOperations," Anagold Madencilik, https://www.anagold.com.tr/en/oxide-operations.

[60] "LidyaMadencilik," Çalık Holding, https://calik.com/en/sectors/mining-sector/lidya-madencilik.

[61] Martin Laryš andKarel Svoboda, "Delegation of Economic Statecraft to Private Enterprises:Russia, China, and Turkey in Africa," International Studies Review26, no. 1 (March 2024): viae009, https://doi.org/10.1093/isr/viae009.

[62] Abdullah Bozkurt,"From Ankara to Wall Street: The Political Shielding and Global Fallout ofTurkey's Mine Disaster," Nordic Monitor, November 13, 2025, https://nordicmonitor.com/2025/11/from-ankara-to-wall-street-the-political-shielding-and-global-fallout-of-turkeys-mine-disaster/.

[63] "TrackingImplementation of NIS Recommendations: Turkey," TransparencyInternational, https://www.transparency.org/en/nis/countries/turkey.

[64] "Türkiye,"WJP Rule of Law Index 2025, World Justice Project, https://worldjusticeproject.org/rule-of-law-index/country/2025/T%C3%BCrkiye/.

[65] "Tracking Implementation of NIS Recommendations: Turkey,"Transparency International, https://www.transparency.org/en/nis/countries/turkey.

[66] "2023Investment Climate Statements: Türkiye," U.S. Department of State, 2023, https://www.state.gov/reports/2023-investment-climate-statements/turkiye.

[67] Akhras v. SSRMining Inc., No. 1:24-cv-00739 (D. Colo., filed March18, 2024), https://www.courtlistener.com/docket/68362592/akhras-v-ssr-mining-inc/.

[68] Akhras v. SSRMining Inc., No. 1:24-cv-00739 (D. Colo., filed March18, 2024), https://www.courtlistener.com/docket/68362592/akhras-v-ssr-mining-inc/.

[69] John Paul Rathbone,"Crackdown or Capital Grab? Turkey State Fund Controls 1,000Businesses," Financial Times, October 15, 2025, https://www.ft.com/content/5c1382f3-cb3e-4a32-8a95-efac9317e9cd.

[70] "Kayyım OlunanŞirketler," Tasarruf Mevduatı Sigorta Fonu (TMSF), last updated May 18,2026, https://www.tmsf.org.tr/tr/Sirket/Kayyim.

[71] AbdullahBozkurt, "Turkey Prepares for Trade Wars with Secret Subsidies to TurkishBusinesses," Nordic Monitor, January 16, 2025, https://nordicmonitor.com/2025/01/turkey-prepares-for-trade-wars-with-secret-subsidies-to-turkish-businesses/.

[72] Kazim Alam,"How Türkiye Plans to Become a Big Player in Global Rare Earth ElementsMarket," TRT World, October 24, 2025, https://www.trtworld.com/article/c8e60f04ebcb.

[73] "TürkiyeTargets 120,000 MW in Wind and Solar by 2035: Minister," Hürriyet DailyNews, November 27, 2025, https://www.hurriyetdailynews.com/turkiye-targets-120-000-mw-in-wind-and-solar-by-2035-minister-216199.

[74] Celal Erbay,"Türkiye'nin Nadir Toprak Elementleri Stratejik Olarak Neden Önemli?"AnadoluAjansı, February 7, 2025, https://www.aa.com.tr/tr/analiz/turkiyenin-nadir-toprak-elementleri-stratejik-olarak-neden-onemli/3474854.

[75] Christina Lu,"America's Military Runs on Chinese Rare Earths," Foreign Policy,August 11, 2025, https://foreignpolicy.com/2025/08/11/china-rare-earths-us-defense-military-pentagon-supply-chain/.

[76] Victor Loh,"China 'Not Afraid of Trade War,' Accuses U.S. of 'Double Standard' forRare Earths Retaliation," CNBC, October 12, 2025, https://www.cnbc.com/2025/10/12/china-defends-rare-earth-export-curbs-as-legitimate-hits-back-at-us-tariffs-ahead-of-possible-trump-xi-meeting.html.

[77] Gracelin Baskaranand Meredith Schwartz, "Developing Rare Earth Processing Hubs: AnAnalytical Approach," Center for Strategic and International Studies, July28, 2025, https://www.csis.org/analysis/developing-rare-earth-processing-hubs-analytical-approach.

[78] MP Materials Corp.,Form 8-K, filed July 9, 2025, U.S. Securities and Exchange Commission, https://www.sec.gov/Archives/edgar/data/1801368/000119312525157310/d43796d8k.htm.

[79] Tasneem Bulbulia,"Pensana Secures $160m Loan Facility for Angola Rare Earths Project,"Mining Weekly, January 23, 2025, https://www.miningweekly.com/article/pensana-secures-160m-loan-facility-for-angola-rare-earths-project-2025-01-23.

[80] "UK RE Hopes Dashedas Saltend Refinery Scrapped," Argus Media, October 17, 2025, https://www.argusmedia.com/en/news-and-insights/latest-market-news/2743508-uk-re-hopes-dashed-as-saltend-refinery-scrapped.

[81] "Critical RawMaterials Act," European Commission, Directorate-General for InternalMarket, Industry, Entrepreneurship and SMEs, https://single-market-economy.ec.europa.eu/sectors/raw-materials/areas-specific-interest/critical-raw-materials/critical-raw-materials-act_en.

[82] "GlobalGateway," European Commission, https://commission.europa.eu/topics/international-partnerships/global-gateway_en.

[83] "Incentive forCritical Minerals Production and Processing in Australia," AustralianGovernment Department of Industry, Science and Resources, February 14, 2025, https://www.industry.gov.au/news/incentive-critical-minerals-production-and-processing-australia.

[84] Patrick Schröder,"Why Rare Earths Are About to Cost a Lot More," Foreign Policy,October 27, 2025, https://foreignpolicy.com/2025/10/27/rare-earths-price-export-controls/.

[85] Selcan Hacaoglu,Firat Kozok, and Patrick Sykes, "Turkey Eyes US Rare Earths Deal AfterChina, Russia Talks Slow," Bloomberg, October 6, 2025, https://www.bloomberg.com/news/articles/2025-10-06/turkey-eyes-us-rare-earths-deal-after-china-russia-talks-slow.

[86] "MineralsSecurity Partnership Forum," European Commission, Directorate-General forTrade, https://policy.trade.ec.europa.eu/help-exporters-and-importers/accessing-markets/raw-materials/minerals-security-partnership-forum_en.

[87] Selcan Hacaoglu, FiratKozok, and Patrick Sykes, "Turkey Eyes US Rare Earths Deal After China,Russia Talks Slow," Bloomberg, October 6, 2025, https://www.bloomberg.com/news/articles/2025-10-06/turkey-eyes-us-rare-earths-deal-after-china-russia-talks-slow.

[88] Nadir Elementler ve Türkiye'nin Beylikova Keşfi (Istanbul: Kuveyt Türk Yatırım, October 21,2025), https://kuveytturkyatirim.com.tr/media/ipej0smq/nadir-elementler-ve-tuerkiyenin-beylikova-ke%C5%9Ffi.pdf.

[89] Didi Bostock, "Unsustainable Prices Hit Rare Earths ProjectsWorldwide," Benchmark Mineral Intelligence, September 3, 2024, https://source.benchmarkminerals.com/article/unsustainable-prices-hit-rare-earths-projects-worldwide.

[90] Kazim Alam, "How Türkiye Plans to Become a Big Player in GlobalRare Earth Elements Market," TRT World, October 24, 2025, https://www.trtworld.com/article/c8e60f04ebcb.

[91] Bonnie S. Glaser andPenny Naas, "Rare Earth Statecraft Phase Two," German Marshall Fundof the United States, October 15, 2025, https://www.gmfus.org/news/rare-earth-statecraft-phase-two.

[92] Gracelin Baskaran, "What China's Ban on Rare Earths ProcessingTechnology Exports Means," Center for Strategic and International Studies,January 8, 2024, https://www.csis.org/analysis/what-chinas-ban-rare-earths-processing-technology-exports-means.

[93] Gracelin Baskaran,"China's New Rare Earth and Magnet Restrictions Threaten U.S. DefenseSupply Chains," Center for Strategic and International Studies, October 9,2025, https://www.csis.org/analysis/chinas-new-rare-earth-and-magnet-restrictions-threaten-us-defense-supply-chains.

[94] "MinisterBayraktar Signed in China," Republic of Türkiye Ministry of Energy andNatural Resources, October 16, 2024, https://enerji.gov.tr/news-detail?id=21379.

[95] Selcan Hacaoglu,Firat Kozok, and Patrick Sykes, "Turkey Eyes US Rare Earths Deal AfterChina, Russia Talks Slow," Bloomberg, October 6, 2025, https://www.bloomberg.com/news/articles/2025-10-06/turkey-eyes-us-rare-earths-deal-after-china-russia-talks-slow.

[96] Ryan Charles,"China's Rare Earth Export Controls and the Repricing of Supply Chains:What It Means for Western Producers and Investors," Crux Investor,October 22, 2025, https://www.cruxinvestor.com/posts/chinas-rare-earth-export-controls-and-the-repricing-of-supply-chains-what-it-means-for-western-producers-and-investors.

[97] Arendse Huld,"How Will China's Rare Earth Export Controls Impact Industries andBusinesses?" China Briefing, November 10, 2025, https://www.china-briefing.com/news/chinas-rare-earth-export-controls-impacts-on-businesses/.

[98] Ryan Charles,"China's Rare Earth Export Controls and the Repricing of Supply Chains:What It Means for Western Producers and Investors," Crux Investor,October 22, 2025, https://www.cruxinvestor.com/posts/chinas-rare-earth-export-controls-and-the-repricing-of-supply-chains-what-it-means-for-western-producers-and-investors.

[99] Başak Erkalan,"Enerji Bakanı Bayraktar: Beylikova'nın Dünyadaki En Büyük Nadir ToprakElementleri Yataklarından Olduğuna İnanıyoruz," Anadolu Ajansı,April 28, 2026, https://aa.com.tr/tr/ekonomi/enerji-bakani-bayraktar-beylikovanin-dunyadaki-en-buyuk-nadir-toprak-elementleri-yataklarindan-olduguna-inaniyoruz/3920302.

[100] Alparslan Bayraktar,Written Parliamentary Question Response, Case No. 7/37054, Republic of TürkiyeMinistry of Energy and Natural Resources, January 8, 2026, https://cdn.tbmm.gov.tr/KKBSPublicFile/D28/Y4/T7/WebOnergeMetni/5fe97cbb-ab7d-4eb9-bd17-4bdb57f44533.pdf.

[101] Patrick Schröder,"Why Rare Earths Are About to Cost a Lot More," Foreign Policy,October 27, 2025, https://foreignpolicy.com/2025/10/27/rare-earths-price-export-controls/.

[102] Arman Sidhu,"Filling the Vacuum: China's Graphite Strategy in NorthernMozambique," Institute for Diplomacy and Economy (instituDE), March 30,2026, https://www.institude.org/opinion/filling-the-vacuum-chinas-graphite-strategy-in-northern-mozambique.