Pakistan is not a party to the U.S.–Iran confrontation, yet it is already paying one of its heaviest economic prices. The oil shock was merely the trigger. Pakistan's structural dependence on Hormuz-transiting petroleum supplied the mechanism through which a geopolitical confrontation it did not initiate became a domestic emergency it cannot easily resolve.

Islamabad’s predicament offers a harder lesson than simple oil dependency: even a recovering economy, genuinely improving under disciplined external management, can have two years of hard-won gains threatened in weeks by a geopolitical decision made in Washington or Tel Aviv.

The Hormuz Shock: When Geography Becomes Destiny

The Strait of Hormuz — a twenty-one-mile passage between Iran and Oman — is the single most consequential energy chokepoint on earth. The EIA states approximately 20.9 million barrels per day transited the Strait in H1 2025 — roughly one-fifth of global petroleum consumption and more than one-quarter of seaborne oil trade.

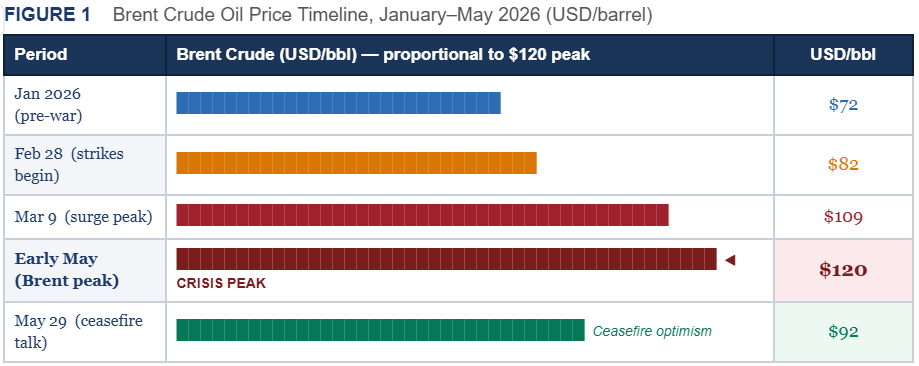

When U.S. and Israeli forces struck Iran on February 28, 2026, the oil market reaction was immediate and historic. Brent crude surged from approximately $72 per barrel to a peak of nearly $120 — a gain of over 55 percent in eleven days. Partial ceasefire talks in late May brought Brent back to $92.56, but infrastructure damage and security uncertainty ensured the energy shock remained far from resolved. Saudi Arabia's East–West Petroline (capacity: 7 mb/d) and the UAE's ADCOP pipeline (capacity: 1.8 mb/d) together offer a combined nameplate ceiling of 8.8 million barrels per day — still less than half of normal Hormuz throughput.

Pakistan is among the Asian economies most severely affected by the closure of the Hormuz Strait. It sources around 81% of its oil imports from the Persian Gulf. Beyond oil, Pakistan and Bangladesh together imported almost two-thirds of their total LNG via the Strait in 2025, with no viable diversification buffer.

Economic Fragility as an Amplifier

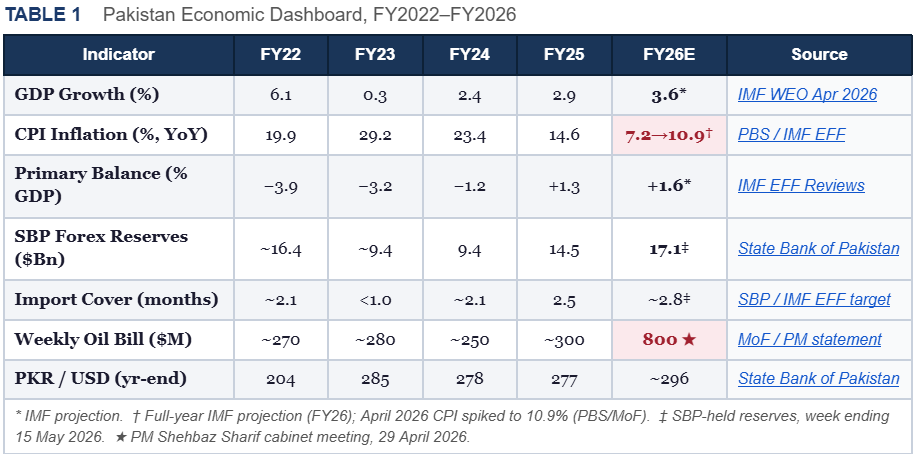

By end-2025, Pakistan had achieved something rare: two consecutive years of macroeconomic stabilization under the IMF's $7 billion Extended Fund Facility approved in September 2024. GDP growth had accelerated to 3.6 percent; the primary fiscal surplus stood at 1.6 percent of GDP — the first sustained surplus in years; gross reserves had been rebuilt to $17.08 billion by mid-May 2026. Headline inflation, which peaked at 29.2 percent in FY2023, had cooled to an IMF projection of 7.2 percent for FY2026. The trajectory was hard-won.

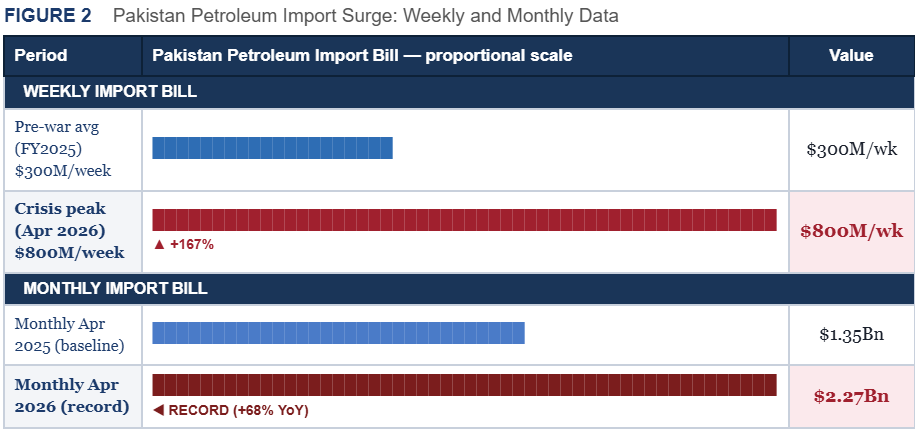

Then the oil shock arrived with structural force. Prime Minister Shehbaz Sharif confirmed on April 29, 2026 that Pakistan's weekly petroleum import bill had surged from $300 million to $800 million — a 167 percent increase. Petroleum group imports hit a record $2.27 billion in April 2026, against $1.354 billion in April 2025 — a 68 percent year-on-year increase that, if sustained, would add more than $11 billion to the annual import burden. Petroleum products already account for more than 22 percent of Pakistan's total import bill; at crisis prices, that share becomes structurally destabilizing.

Unable to absorb the additional cost, the government introduced two-hour daily power cuts and a four-day working week. The IMF accelerated a $1.3 billion disbursement in May 2026 to help finance surging import costs — the third review tranche deployed against an energy emergency rather than a reform milestone. Revised projections cut Pakistan's FY2027 GDP growth forecast to 3.5 percent and raised the inflation projection to 8.4 percent. Two years of discipline, partially undone in weeks.

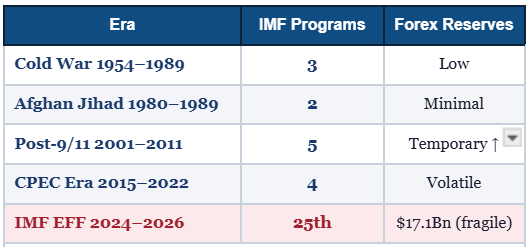

The immediate shock was external, but the vulnerability that turned it into a national economic emergency had been accumulating for decades. Across seven decades and twenty-five IMF programs, external flows have repeatedly arrived in an emergency and departed without resolving the structural conditions that produced it — as Figure 3 documents.

FIGURE 3 Pakistan's 25 IMF Programs (1958–2026) vs. Structural Reform Outcomes

Islamabad's Iran Dilemma: A Structural Trap

Cornered by an import bill it cannot finance within existing constraints, Islamabad activated six overland trade corridors connecting Karachi, Port Qasim, and Gwadar to Iranian border crossings at Taftan and Gabd — cutting transport costs by up to 45–55 percent relative to maritime alternatives.

This overland route to Iran offers real cost relief — but activating it risks drawing Pakistan into transactions with a state under comprehensive U.S. sanctions. The U.S. Treasury's Office of Foreign Assets Control (OFAC) has repeatedly designated banks, shipping intermediaries, and trade facilitators accused of enabling Iranian commercial access. Pakistan’s commercial banks, which depend on U.S. dollar correspondent relationships for international trade settlement, are therefore acutely exposed to any OFAC warning or designation. At the same time, IMF EFF conditionalities constrain fiscal maneuver, leaving Islamabad dependent on multilateral support that no bilateral trade corridor with Iran can offset.

Islamabad cannot alienate Washington without losing access to the dollar-based financial architecture on which its economy depends. It cannot ignore Tehran without forfeiting one of the few supply corridors capable of partially mitigating a shock generated, in material part, by Washington's strategic decisions. The immediate shock is of no Pakistani making. The resolution will be Pakistan's alone to navigate — with diminishing flexibility and diminishing time.